Jean Bovin – Head of BlackRock Investment Institute together with Wei Li – Global Chief Investment Strategist, Alex Brazier – Deputy Head, and Nicholas Fawcett – Macro Research all forming part of the BlackRock Investment Institute, share their insights on global economy, markets and geopolitics. Their views are theirs alone and are not intended to be construed as investment advice.

Key Points

Flip flops: Market narratives have flip-flopped through the year as the new macro regime plays out. We stay selective amid stagnating activity and volatile inflation.

Market backdrop: U.S. stocks dipped and bond yields climbed after solid U.S. services data. Markets are coming around to our view of key central banks holding policy tight.

Week ahead: U.S. CPI data this week should show more post-pandemic normalization. We see inflation on a rollercoaster ride ahead as an aging population starts to bite.

We‘re in an unprecedented macro environment that is driving constant shifts in the market narrative: from hopes of avoiding recession to fears good macro news could be bad for markets in just a few months. We see the market moving with data as if we’re in a normal business cycle. But we’re in a new regime, with pandemic disruptions giving way to structural shifts that are playing out now, like an aging workforce. We see opportunities from timing market swings and staying selective.

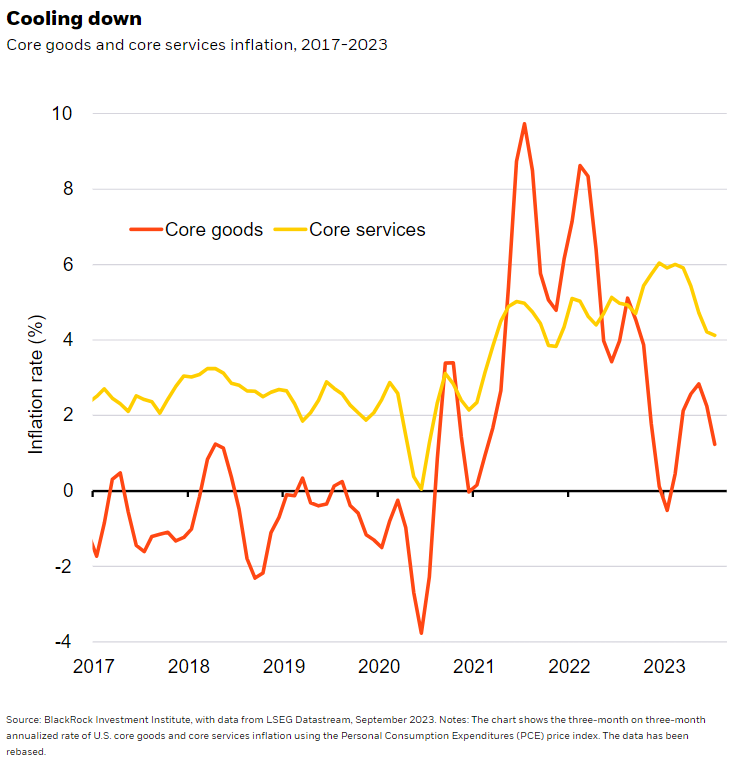

Inflation is likely to keep falling as pandemic mismatches resolve. See the chart. Core goods prices have seen the sharpest drop (dark orange line) as consumers shifted spending back toward services after splurging on goods during the pandemic. We estimate that about two-thirds of the spending shift has now unwound. At the same time, the spike in job openings is normalizing without a rise in unemployment. That has helped ease wage growth – leading to lower price pressure in core services as well (yellow line). Employers in leisure and retail, for example, now face less pressure to pay up for the workers they needed that were in short supply. Shifting narratives show how the market is trying to translate an assessment of the inflation and broader macro picture into investment views based on a typical business cycle. But we think mapping the macro outlook to markets is less straightforward in the new regime.

Euphoria over artificial intelligence (AI) has buoyed U.S. equities this year even with the tough macro backdrop. The bank turmoil in March revived recession fears, but equities soon resumed a climb and gained steam on falling inflation. By August, stocks stalled. Data suggesting solid growth spurred fears of higher-for-longer rates – “good news” became “bad news” – and bond yields surged as investors started demanding more term premium for the risk of holding long-term bonds.

Stealth stagnation

We think the narrative could flip again. A key part of the story has gone under the radar: stagnation. The economy has already stagnated for 18 months when taking the average of GDP and gross domestic income, according to U.S. Bureau of Economic Analysis data. Outright recession has so far been avoided and Q3 growth looks set to pick up, thanks to consumers spending their pandemic savings. But as savings are exhausted, next year could bring lower growth. Recession is still in the cards. But whether we go through recession and recovery, or flatlining activity, we think we end up in the same place. However we get there, it would mean the weakest two-and-a-half years for the U.S. economy outside the global financial crisis. So how has weak growth gone under the radar? One reason: Seemingly strong job growth largely reflects a catch-up from the pandemic shock. Adjusting for that, it’s been quite weak – and still worker shortages persist due to an aging population. With the job catch-up nearly complete, employment growth is slowing, we find. This sets up another potential narrative flip as stagnation sinks in. Take Europe. Activity has weakened and may be in recession. As a result, the early outperformance of European stocks this year has fizzled. And the European Central Bank may pause its rate hikes this week.

More broadly, all these market narratives apply a typical business cycle lens. We think the core issue is structural and playing out now. The labor force is growing more slowly as the population ages. Weak growth doesn’t translate into higher unemployment like it used to: We see full-employment stagnation. Demographic shifts causing worker shortages mean inflation can only be kept low with weaker growth, in our view. As labor shortages start to bind, we think inflation pressures could build again, putting inflation on a rollercoaster ride and compelling major central banks to hold policy tight.

Bottom line

Markets can run with narratives a while before flipping, creating potential for market-timing opportunities with the swings. We stay nimble and selective in stocks and credit. We underweight the broad market of developed market equities on a six- to 12-month horizon. And over that horizon, we look to harness mega forces like AI to tap structural drivers shaping returns now and in the future.

Market backdrop

U.S. stocks fell more than 1%, coming under pressure as 10-year Treasury yields pushed back near 16-year highs and markets priced out some of the Federal Reserve rate cuts seen next year. This week’s narrative was again “good news is bad news” – U.S. services activity topped expectations in August, reinforcing the higher-for-longer view on policy rates. European stocks hit six-month lows as grim German industrial production data highlighted the euro area’s potential recession.

U.S. CPI inflation data takes center stage this week. Inflation has fallen as pandemic-driven mismatches have reversed. We see inflation on a rollercoaster ride ahead as that process ends and an aging population constrains the workforce. In Europe, falling inflation and slowing economic activity will likely lead the ECB to hold policy rates steady this week.

Week Ahead

Sept. 12: UK labor market data

Sept. 13: U.S. CPI

Sept. 14: European Central Bank (ECB) policy decision

Sept. 15: University of Michigan consumer sentiment survey

BlackRock’s Key risks & Disclaimers:

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of 11th September, 2023 and may change. The information and opinions are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This material may contain ’forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation. Investment involves risk including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are often heightened for investments in emerging/developing markets or smaller capital markets.

Issued by BlackRock Investment Management (UK) Limited, authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from BlackRock Investment Management (UK) Limited. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Information Document (KID), which may be obtained from MeDirect Bank (Malta) plc.