Wei Li – Global Chief Investment Strategist, together with Alex Brazier – Deputy Head, Nicholas Fawcett – Macro research, and Ann-Katrin Petersen – Senior Investment Strategist all forming part of the BlackRock Investment Institute, share their insights on global economy, markets and geopolitics. Their views are theirs alone and are not intended to be construed as investment advice.

Key Points

No ignoring trade-off: Central banks confront the growth-inflation trade-off, with the Federal Reserve seeing recession but no rate cuts. We agree – and prefer inflation-linked bonds.

Market backdrop: Bank stocks remained under pressure last week. The two-year U.S. Treasury yield slid further as the market priced in a series of Fed rate cuts.

Week ahead: We’re watching inflation data on both sides of the Atlantic this week for further signs of it staying elevated, while monitoring the ongoing banking sector woes.

The central bank trade-off between crushing activity or living with inflation is now impossible to ignore as economic damage and financial cracks emerge. That was evident in the Federal Reserve’s forecast of recession this year and sticky inflation in years to come. Central banks have clearly separated responses to the banking tumult and kept hiking rates. We see a new, more nuanced phase of curbing inflation ahead: less fighting but still no rate cuts. We favor inflation-linked bonds.

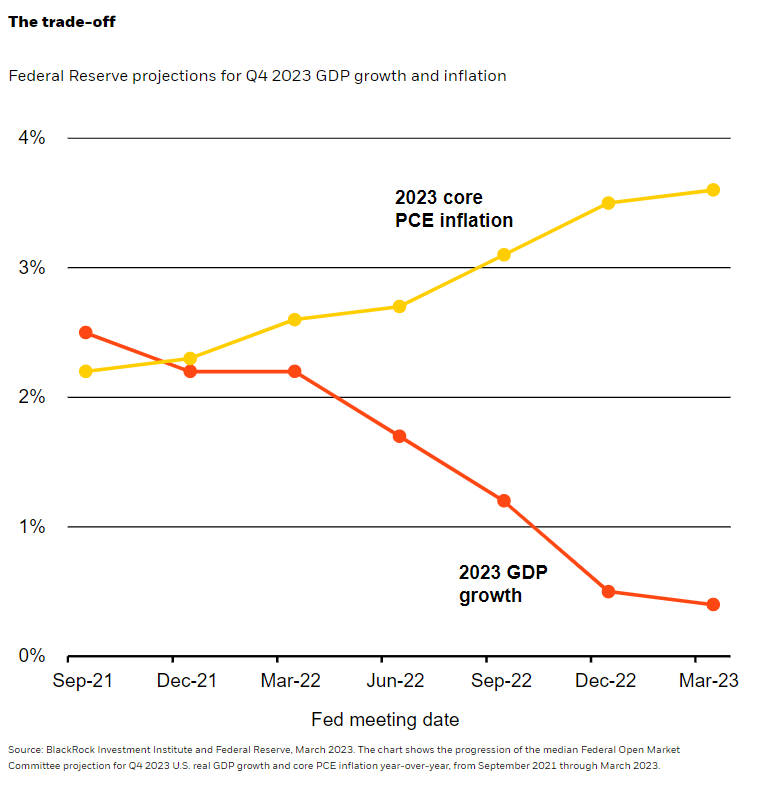

The progression of the Fed’s forecasts shows it has been repeatedly too optimistic on both growth and inflation – that’s the trade-off in action. See the chart. Its latest projections imply a recession in the months ahead, with growth stalling later in 2023 after a strong start to the year (red line). The Fed still doesn’t plan to cut rates because inflation is persistently above its 2% target. So it is expecting to live with lingering inflation even with recession – it sees PCE inflation remaining above 3% at the end of 2023 (yellow line). It doesn’t see inflation falling back near its target until 2025. Even so, we think the Fed is underestimating how stubborn inflation is proving due to a tight labor market: Inflation could remain above its target for even longer than that if the recession is as mild as the Fed projects.

The Fed and other central banks made clear banking troubles would not stop them from further tightening. U.S. authorities acted swiftly to help stem contagion by protecting depositors from bank failures. By clearly separating financial and price stability goals and tools, major central banks carried on with rate hikes through the tumult. The Fed, European Central Bank and the Bank of England all did so. Even the Swiss National Bank lifted rates by 0.5% just days after facilitating a takeover of long-troubled Credit Suisse. The bank troubles imply higher borrowing costs and tighter credit availability – and are part of the economic and financial damage we’ve long argued would come. That damage is now front and center – central banks are finally forced to confront it. We think this means they are set to enter the new phase of curbing inflation that we’ve been flagging. We see major central banks moving away from a “whatever it takes” approach, stopping their hikes and entering a more nuanced phase that’s less about a relentless fight against inflation but still one where they can’t cut rates.

No rate cuts this year

Markets have been quick to price in rate cuts as a result of the banking sector turmoil and the Fed signaling a coming pause. We don’t see rate cuts this year – that’s the old playbook when central banks would rush to rescue the economy as recession hit. Now they’re causing the recession to fight sticky inflation – and that makes rate cuts unlikely, in our view. Stocks have held up due to hopes for rates cuts that we don’t see coming. We think the Fed could only deliver the rate cuts priced in by markets if a more serious credit crunch took hold and caused an even deeper recession than we expect. We stay underweight developed market (DM) stocks because we don’t think they reflect the damage we see ahead.

Inflation is likely to prove even stickier than the Fed expects without a deep recession, in our view. The February U.S. CPI data confirmed our view that inflation is still not on track to settle at the Fed’s target. Current market pricing of U.S. and euro area inflation just above 2% on a 10-year horizon has edged lower recently – we think levels are likely to stay much higher than that. This is why we see value in inflation-linked bonds and prefer them to nominal peers. We also find very short-term government paper attractive for income given the potential for the market to price out rate cuts quickly. Strong money market demand provides additional support, in our view. We’re underweight long-term government bonds as we see yields rising with investors demanding more compensation for holding them, or term premium, given persistent and volatile inflation.

Bottom line

We overweight inflation-linked bonds and like very short-term government paper for income. We stay nimble in the new regime of greater macro and market volatility – and are ready for opportunities as rate-hike damage gets priced in.

Market backdrop

U.S. and Europe stocks steadied, even as bank and financial shares remained under pressure. Some European bank default protection costs jumped on the week. The U.S. two-year Treasury yield extended its historic drop and is down about 1.4 percentage points from a 16-year high hit earlier this month, causing a further steepening of the yield curve. The market is now pricing in about 1 percentage point of Fed rate cuts by the end of the year. We don’t think such cuts are coming.

We’re watching inflation on both sides of the Atlantic – including the Fed’s preferred PCE inflation gauge and flash inflation in the euro area. We expect services inflation to keep core inflation elevated. We’re watching U.S. consumer confidence as well for more signs of damage from still-rising rates, sticky inflation and banking sector troubles.

Week Ahead

Mar 28: U.S. consumer confidence

Mar 31: U.S. PCE inflation and spending; euro area inflation and unemployment

BlackRock’s Key risks & Disclaimers:

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of 27th March, 2023 and may change. The information and opinions are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This material may contain ’forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation. Investment involves risk including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are often heightened for investments in emerging/developing markets or smaller capital markets.

Issued by BlackRock Investment Management (UK) Limited, authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from BlackRock Investment Management (UK) Limited. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Information Document (KID), which may be obtained from MeDirect Bank (Malta) plc.