Jean Boivin, Head of the BlackRock Investment Institute, together with Wei Li, Global Chief Investment Strategist, Alex Brazier, Deputy Head, and Nicholas Fawcett, Macro research, all forming part of the BlackRock Investment Institute, share their insights on global economy, markets and geopolitics. Their views are theirs alone and are not intended to be construed as investment advice.

Key Points

Central bank conundrum: Many central banks aren’t acknowledging the extent of recession needed to rapidly reduce inflation. Markets haven’t priced that so we shun most stocks.

Market backdrop: Yields surged after more rate hikes and the UK’s fiscal splurge news. We cut UK gilts to underweight as we see higher rates and fiscal credibility questions.

Week ahead: U.S. and euro area inflation are likely to show persistence in data this week. We think central banks underestimate the cost of bringing it down to target quickly.

Many central banks, like the Fed, are still solely focused on pressure to quickly get core inflation back to 2% without fully acknowledging how much economic pain it will take in a world shaped by production constraints. Case in point: last week’s rate-hike blitz. This all implies a clear sequence: overtighten policy first, significant economic damage second and then signs of inflation easing only many months later. We’re tactically underweight developed market (DM) stocks and prefer credit.

Rapid rate rises

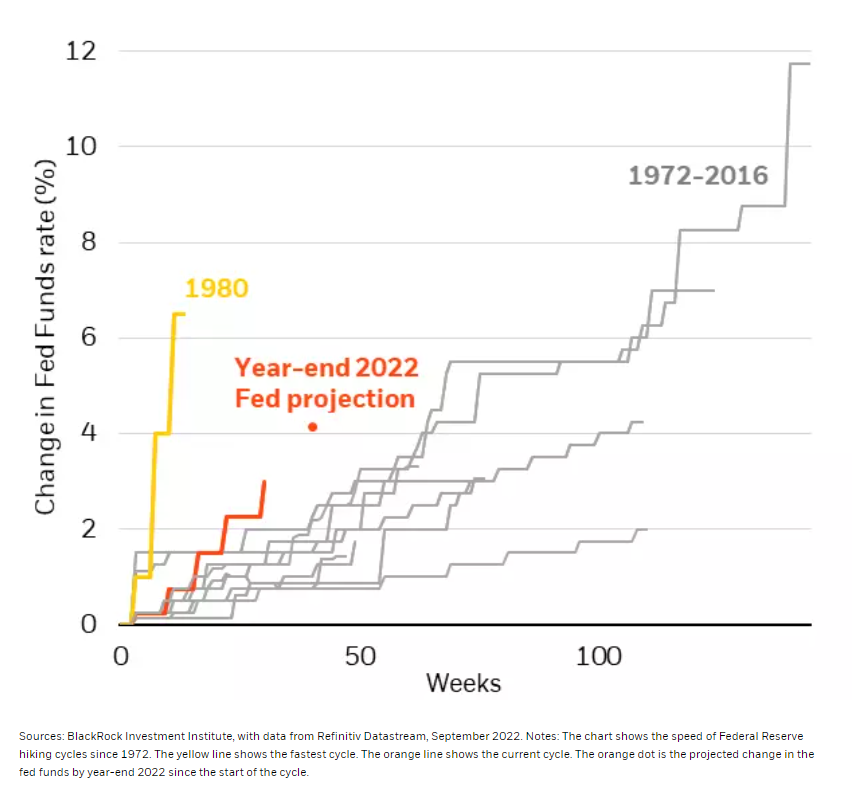

U.S. interest rate tightening cycles, 1972-2022

The Federal Reserve is on its fastest rate hiking cycle since the early 1980s (see orange and yellow lines in chart). It hiked another 0.75% last week and projected rates would go even higher. The Fed now sees the fed funds rate rising to 4.6% by the end of 2023, a significant bump from prior views. The problem? Updated economic forecasts are too optimistic, in our view. The Fed still sees positive growth this year and sees it picking up next year. But it also wants to see evidence core inflation is on a decisive 2% trajectory beyond 2023 before it stops hiking. This soft landing doesn’t add up to us. We think quashing inflation that quickly amid constrained production capacity would take a recession – a roughly 2% hit to economic activity and 3 million more unemployed. We think the Fed is not only underestimating the recession needed but ignoring that it’s logically necessary.

Why would a recession be needed to reduce core inflation? Unusually low supply can’t meet demand. That’s driving inflation. There are two reasons why. First, a labor shortage – people who left the workforce during the pandemic haven’t returned yet. Second, the economy wasn’t set up to match consumer spending’s massive shift from services to goods that hasn’t fully reversed even as the world moves on from the pandemic. Central banks can’t fix these constraints, in our view, hence a brutal trade-off: trigger a deep recession by hiking rates or live with more persistent inflation. The Fed’s forecasts don’t acknowledge this trade-off. It reconciles this by assuming production constraints will rapidly dissolve, causing inflation to fall quickly. But if that’s the outcome, what’s the point of the fastest hiking cycle since former Fed Chair Paul Volcker’s era?

The case of the UK

The Bank of England (BoE) has been transparent that quickly pushing inflation down will require a recession. But the UK now faces different challenges that change fundamentally how we look at UK assets. The UK government revealed a fiscal splurge on Friday that effectively throws money at an inflation problem, in our view. After last week’s hike, this means the BoE will have to hike more and leave rates elevated for longer than it planned to, we think. But more importantly, the fiscal splurge puts the UK’s fiscal credibility into question. The plans follow measures to subsidize energy bills and amount overall to 10% of GDP over the next five years, we estimate. The pound cratered to a 37-year low against the dollar and gilt yields surged after the news. All of this will help motivate the BoE’s hawkishness. That’s why we’ve downgraded UK gilts to underweight.

Central bank implications

The implications of all of this: We think central banks will keep raising rates until it’s clear that core inflation is coming down. That means economic activity is set to fall across DMs. The Fed’s current policy may drag down U.S. growth far more than it realizes. In Europe, we see the European Central Bank’s resolve to push inflation down fraying as it wakes up to the bleak outlook. But that reaction will come too late to prevent the central bank from amplifying the energy shock’s recessionary forces, in our view. The continent will see a deeper recession than in the U.S.

Our bottom line

We’re tactically underweight DM equities as stocks aren’t fully pricing in recession risks. We don’t see a “soft landing” outcome where inflation returns to target quickly without crushing activity. That means more volatility and pressure on risk assets, we think. We prefer investment grade credit as yields better compensate for default risk. Plus, high quality credit can weather a recession better than stocks. We find inflation-linked bonds more attractive and stay cautious on long-term nominal government bonds amid persistent inflation.

Market backdrop

Stocks slid and yields surged after hawkish central bank actions. The Fed raised rate expectations into next year and revised growth and unemployment forecasts. We think they’re too optimistic. The Bank of England also hiked. But a fiscal splurge may lead to even more hikes and poses risks of further rises in long-term yields and pound depreciation. Japan intervened for the first time since 1998 to prop up the yen. Bucking the trend, the Bank of Japan kept its yield curve control policy.

We’re watching inflation data in the U.S. and the euro area, including the Fed’s preferred PCE metric. For now, the Fed only seems to care about evidence inflation is decisively on a path toward its 2% target. The assessment of U.S. consumers will show if they agree with Fed forecasts that the economy can avoid recession. We think the Fed is underappreciating the economic damage needed to bring inflation down quickly to target. We see persistent inflation and recession next year in the U.S.

Week Ahead

Sept. 27: U.S. consumer confidence and durable goods

Sept. 29: Bank of Mexico policy decision

Sept. 30: U.S. PCE and euro area HICP inflation; China PMI; UK GDP

BlackRock’s Key risks & Disclaimers:

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of 26th September, 2022 and may change. The information and opinions are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This material may contain ’forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation. Investment involves risk including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are often heightened for investments in emerging/developing markets or smaller capital markets.

Issued by BlackRock Investment Management (UK) Limited, authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from BlackRock Investment Management (UK) Limited. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Investor Information Document (KIID), which may be obtained from MeDirect Bank (Malta) plc.