Jean Boivin – Head of BlackRock Investment Institute together with Wei Li – Global Chief Investment

Strategist, Ben Powell – Chief Investment Strategist for the Middle East and APAC, and Nicholas Fawcett –

Macro Research, all forming part of the BlackRock Investment Institute share their insights on global economy, markets and geopolitics. Their views are theirs alone and are not intended to be construed as investment advice.

Key Points

Cutting, not easing : The Fed is set to cut interest rates for the first time since the pandemic. Yet central banks are not heading for an easy policy stance given sticky inflation.

Market backdrop : U.S. stocks rose about 4% last week, led by tech. U.S. 10-year Treasury yields touched 15-month lows, with markets pricing steep Fed cuts that look overdone.

Week ahead : The Fed policy meeting takes center stage this week. The recent drop in U.S. core CPI stalled in August, likely taking a 50-basis-point cut off the table, in our view.

The Federal Reserve is set to start rate cuts this week after its rapid hikes to rein in inflation. Markets expect the Fed to cut rates sharply – and we think this pricing is overdone. U.S. inflation has slowed as pandemic disruptions have faded and due to a temporary immigration boost to the workforce. We see inflation staying sticky due to loose fiscal policy and the impact of mega forces, limiting how far the Fed can cut. Yet we think recession fears are overdone and stay overweight U.S. stocks.

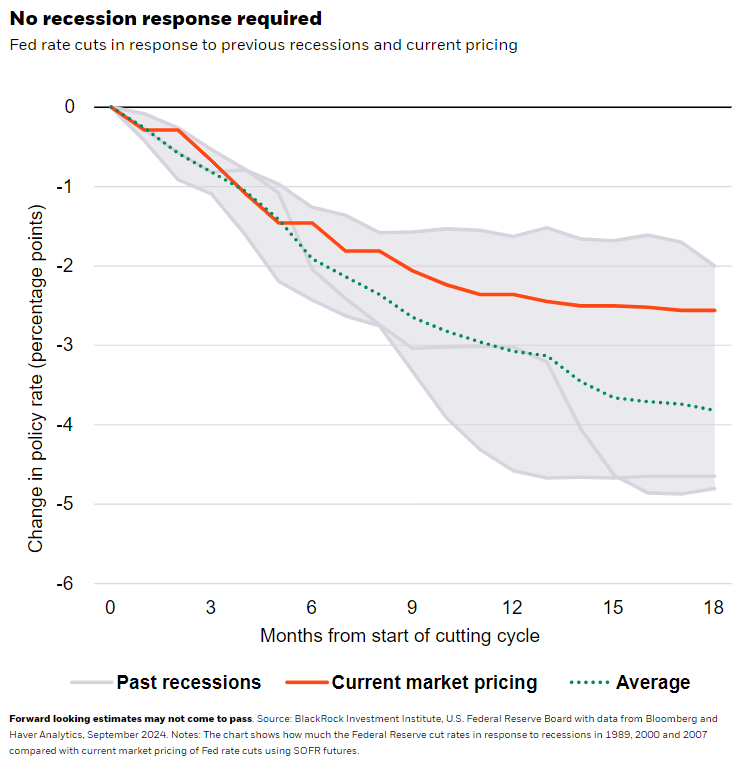

Markets have been quick to price in rate cuts after the Fed finished its fastest hikes since the 1980s – and price them out when inflation spooked to the upside. As the Fed readies to start cutting, markets are pricing in cuts as deep as those in past recessions. See the chart. We think such expectations are overdone. An uptick in the unemployment rate has stoked recession fears, yet employment is still growing. The unemployment rate is not rising due to layoffs, but because elevated immigration has expanded the workforce. Consumer spending shifting back to services from goods after the pandemic has helped inflation fall from its recent highs, allowing the Fed to cut rates. A larger workforce is helping cool services inflation. Yet in this new regime, central banks face a sharper trade-off between curbing inflation and protecting growth than in the decades-long period of steady growth and inflation.

Cooling inflation is likely temporary. The post-pandemic normalization of spending and supply mismatches is largely over, while immigration is likely to fall back to historic trends. Once it does, the economy won’t be able to add jobs as fast as it has been without stoking inflation. Wage growth has slowed but not enough to suggest that core inflation could fall to the 2% target. Supply constraints from mega forces, or structural shifts, are set to add to global inflation pressures. That’s why the Fed and other central banks will keep rates higher for longer. Yet short-term U.S. Treasury yields have slid on expectations for deep rate cuts, so we went underweight. We stay overweight U.S. stocks but broaden our artificial intelligence view beyond tech. Our Midyear Outlook scenarios acknowledge the low odds of the Fed cutting rates as much as markets expect. That could occur if the Fed sees cooling job growth as a sign it’s been too slow to react to worsening growth, echoing its rapid rate hikes. Risk sentiment may sour once it’s clear the Fed won’t cut rates as low as markets expect.

Going global

The European Central Bank (ECB) cut rates again last week even as inflation is above its target for now. We see euro area inflation falling to 2% and staying near there, unlike in the U.S. That’s still far from the low inflation of the past decade. But the ECB tightened policy more than the Fed – even as it faced weaker economic activity – so it has more room to cut rates, in our view. We’re neutral euro area government bonds and UK gilts as market pricing of rate cuts could go further, in our view.

The People’s Bank of China has been cutting rates but it’s not in the same boat as the Fed. It’s facing weak consumer demand, excess production capacity and deflation – based on broad measures of inflation – that could become entrenched. The lack of fiscal and other policy support casts doubt on if the economy will hit this year’s growth target. Export activity has been supporting growth, so it will be key to watch for any signs of weakness. Chinese equity valuations are low relative to other regions but given the tough macro outlook, we prefer developed market equities over emerging markets and China.

Our bottom line

The Fed is following in the footsteps of other central banks to cut rates this week. We see sticky inflation limiting how far central banks can cut. We stay overweight U.S. equities and prefer European over U.S. bonds.

Market backdrop

U.S. stocks rose about 4% last week, rebounding from their largest weekly drop in 18 months, with tech helping lead the way as recession fears faded and on coming Fed rate cuts. U.S. 10-year Treasury yields touched 15-month lows, settling near 3.66% with markets pricing in 200 basis points of Fed cuts by next June. We think this is overdone and could set up more sharp pricing shifts as markets see-saw between starkly different potential outcomes.

Central bank policy meetings take center stage this week, headlined by the Fed. We expect the Fed to cut rates for the first time since its rapid hikes launched in 2022. Yet the recent drop in U.S. core CPI stalled in August, likely taking a 50-basis-point cut off the table, in our view. The BOJ will also be in focus after being a source of market volatility after its last meeting in late July.

Week Ahead

Sept. 18 : Fed policy decision; UK CPI; Japan trade data

Sept. 19 : Bank of England policy decision; Philly Fed business index

Sept. 20 : Bank of Japan policy decision; Japan CPI; euro area consumer confidence

BlackRock’s Key risks & Disclaimers:

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of 16th September, 2024 and may change. The information and opinions are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This material may contain ’forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation. Investment involves risk including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are often heightened for investments in emerging/developing markets or smaller capital markets.

Issued by BlackRock Investment Management (UK) Limited, authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from BlackRock Investment Management (UK) Limited. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document is intended for retail clients however, it may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Information Document (KID), which may be obtained from MeDirect Bank (Malta) plc.