Wei Li, Global Chief Investment Strategist of the BlackRock Investment Institute together with Scott Thiel, Chief Fixed Income Strategist, Axel Christensen, Chief Investment Strategist LatAm & Iberia and Baeta Harasim, Senior Investment Strategist all forming part of the BlackRock Investment Institute, share their insights on global economy, markets and geopolitics. Their views are theirs alone and are not intended to be construed as investment advice.

Key Points:

EM local debt’s appeal: We like emerging market (EM) local debt within an overall bond underweight. Much monetary tightening has been done, and valuations are compelling.

Market backdrop: U.S. Treasury yields hit new three-year highs last week, and equities fell. We still think stocks can weather the yield rise in the inflationary backdrop.

Week ahead: U.S. and euro area data this week may show how the supply shock of the Ukraine war is affecting growth. We expect Europe to be hit harder than the U.S.

Inflation and hawkish central bank talk have spooked investors and led to bond losses not seen since the 1980s in developed markets (DMs). EM debt has also suffered, even ahead of the stress test of higher DM policy rates. The good news: Many EM central banks were early in raising rates to try to rein in inflation. This approach has created compelling yield and currency valuations, in our view. Broad indexes hide a lot of differentiation, so it’s key to analyze the underlying exposures.

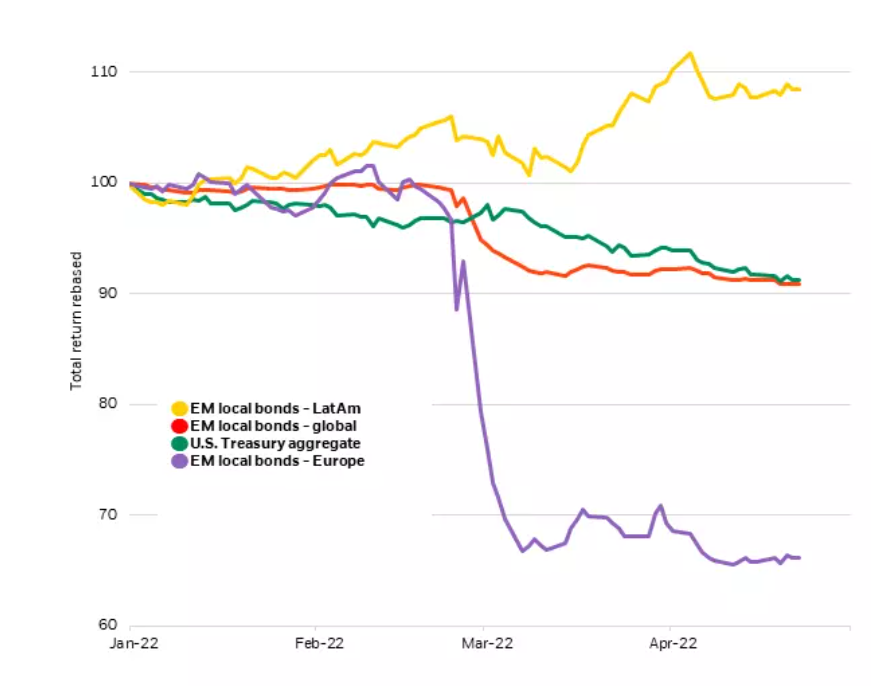

A tale of different EMs

Emerging market local debt vs. U.S. Treasuries total returns, 2022

Past performance is not a reliable indicator of current or future results. Indexes are unmanaged and not subject to fees. It is not possible to invest directly in an index. Sources: BlackRock Investment Institute, with data from Refinitiv, April 2022. Notes: The chart shows the total returns for emerging market local-currency bonds compared with U.S. Treasury bonds based on the JP Morgan GBI-EM Global Diversified and regional (LatAm and Europe) indexes and Bloomberg U.S. Treasury USD index.

It’s been an annus horribilis for bonds everywhere this year – except in some corners of the emerging world. Why? Scarcity inflation has arrived. Supply shocks have created shortages of goods, energy and food that are driving up prices. This has spurred DM central banks to signal faster policy normalization than markets expected and resulted in bond yields rocketing upward. Local-currency EM debt (the red line in the chart) has suffered alongside U.S. Treasuries (green line) so far this year. It’s key to realize broad EM indexes hide a lot of differentiation. Local-currency debt of commodities producers such as Latin America (yellow line) and the Middle East & Africa have actually posted gains this year, outperforming debt of commodities-consuming Asia and Europe (purple line). The latter was directly hit by the fall-out of Russia’s invasion of Ukraine.

Rate hike risk

How about the risk of the Fed’s upcoming rate hikes? This has often spelled trouble for EM assets. Investors have tended to demand a higher risk premium for holding them. Fed tightening also has frequently come with a stronger U.S. dollar, pressuring EM entities with hard-currency borrowings. We see the Fed’s impact as more limited this time. First, the Fed is rightly racing to normalize policy, but we believe it won’t fully deliver on its hawkish rate hike plans in the end. Second, we expect the sum total of rate hikes to be historically low given the level of inflation.

We also see a strong starting position for EM debt, given cheapened EM currencies, improved external balances, decreased foreign ownership and attractive coupon income. The main reason: Many EM central banks have been ahead of the curve in raising interest rates to fight inflation, as we noted in Liftoff? EM has already taken off of November 2021. This means they are much further along on the path to policy normalization than DM central banks. Real yields, or inflation-adjusted yields, have been edging into positive territory in some countries.

What are the risks? DM central banks could push rates to levels that destroy growth in an effort to rein in inflation. This would deal a blow to EM countries already struggling with high import prices of commodities and rising debt piles as a result of COVID relief programs. Alternatively, some EM countries could see runaway inflation, forcing their central banks to slam the brakes. And some could face social unrest in the face of fast-rising prices of food and other basic goods.

It’s important to realize broad EM indexes hide a lot of differentiation. EM equity indexes, for example, are heavily weighted toward Asia. The benchmark GBI EM Diversified local-currency index has a 10% cap on any one sovereign issuer, giving more diversification and exposure to commodities exporters. It also means investors may need to go beyond indexes to get the exposures they are bullish on – and avoid the ones they have little confidence in. EM assets tend to offer fertile ground for security selection, we find, compared with heavily researched asset classes such as DM large-cap equities.

Our Bottom Line

We maintain a modest overweight to EM local-currency debt amid an overall underweight to bonds. Much monetary tightening is already done, and valuations are compelling. We are neutral hard-currency EM debt. It is sensitive to rising U.S. rates, and valuations are now less attractive vis-à-vis U.S. credit. We prefer to take EM risk in debt, rather than equities. We prefer DM stocks because of EM’s challenged restart dynamics, inflation pressures and tighter policies.

Market Backdrop

Yields on 10-year U.S. Treasuries rose to near 3% last week, levels not seen since late 2018. Equities ended down as the first-quarter earnings season gathered steam. We still think stocks can perform even as yields rise in the inflationary backdrop. The IMF forecasts much higher inflation and weaker growth, especially in Europe, due to the supply shock emanating from the Ukraine war. We believe downside risks to growth in China have increased amid Covid lockdowns.

This week’s highlights will be U.S. and euro area inflation and GDP data releases that further reveal the growth impact of the stagflationary supply shock from the war in Ukraine. We expect Europe to feel the hit more than the U.S. China manufacturing data will likely reflect how a spike in COVID cases is restricting activity.

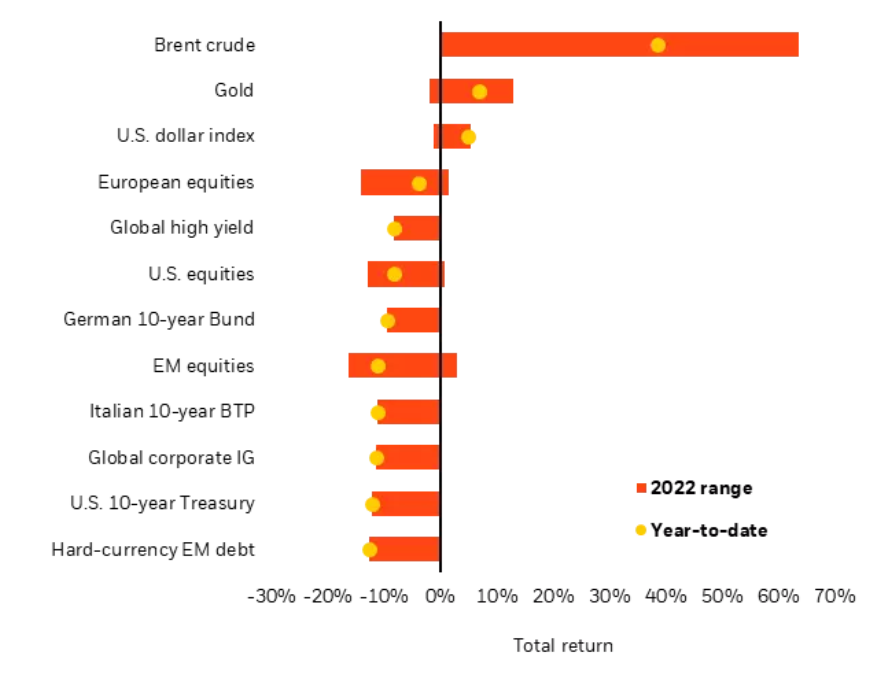

Past performance is not a reliable indicator of current or future results. Indexes are unmanaged and do not account for fees. It is not possible to invest directly in an index. Sources: BlackRock Investment Institute, with data from Refinitiv Datastream as of April 22, 2022. Notes: The two ends of the bars show the lowest and highest returns at any point this year to date, and the dots represent current year-to-date returns. Emerging market (EM), high yield and global corporate investment grade (IG) returns are denominated in U.S. dollars, and the rest in local currencies. Indexes or prices used are: spot Brent crude, ICE U.S. Dollar Index (DXY), spot gold, MSCI Emerging Markets Index, MSCI Europe Index, Refinitiv Datastream 10-year benchmark government bond index (U.S., Germany and Italy), Bank of America Merrill Lynch Global High Yield Index, J.P. Morgan EMBI Index, Bank of America Merrill Lynch Global Broad Corporate Index and MSCI USA Index.

Week Ahead

- April 26: U.S. durable goods and consumer confidence data

- April 28: Germany CPI and HICP; U.S. GDP Q1 Advance; Bank of Japan meets

- April 29: Euro area GDP and HICP Flash; U.S. consumption; Russia central bank meeting

- April 30: China manufacturing PMI

BlackRock’s Key risks & Disclaimers:

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of April 25th, 2022 and may change. The information and opinions are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This material may contain ’forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation. Investment involves risk including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are often heightened for investments in emerging/developing markets or smaller capital markets.

Issued by BlackRock Investment Management (UK) Limited, authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from BlackRock Investment Management (UK) Limited. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Investor Information Document (KIID), which may be obtained from MeDirect Bank (Malta) plc.