Jean Boivin – Head of BlackRock Investment Institute together with Wei Li – Global Chief Investment Strategist, Glenn Purves – Global Head of Macro, and Vivek Paul – Global Head of Portfolio Research all forming part of the BlackRock Investment Institute share their insights on global economy, markets and geopolitics. Their views are theirs alone and are not intended to be construed as investment advice.

Key Points

Leaning short-term : Immutable economic laws offer more certainty in the near term as long-term macro anchors weaken. That, and mega forces, keep us overweight U.S. equities.

Market backdrop : U.S. stocks edged up to record highs on the AI theme. U.S. 10-year yields edged up as June payrolls data beat expectations, a sign sticky inflation will persist.

Week ahead : We are monitoring the expiration of the 90-day suspension of U.S. reciprocal tariffs announced on April 2 and watching for any indications of an extension.

.

Big policy shifts seem to have upended the world this year – but our 2025 Midyear Outlook puts them in perspective. We think immutable economic laws on global trade and U.S. debt limit how quickly the world can change. And while we see long-term macro anchors weakening, we think mega forces like artificial intelligence provide a new anchor. These two core features of this environment keep us risk on and overweight U.S. equities. Watch for more from our Outlook in coming weeks.

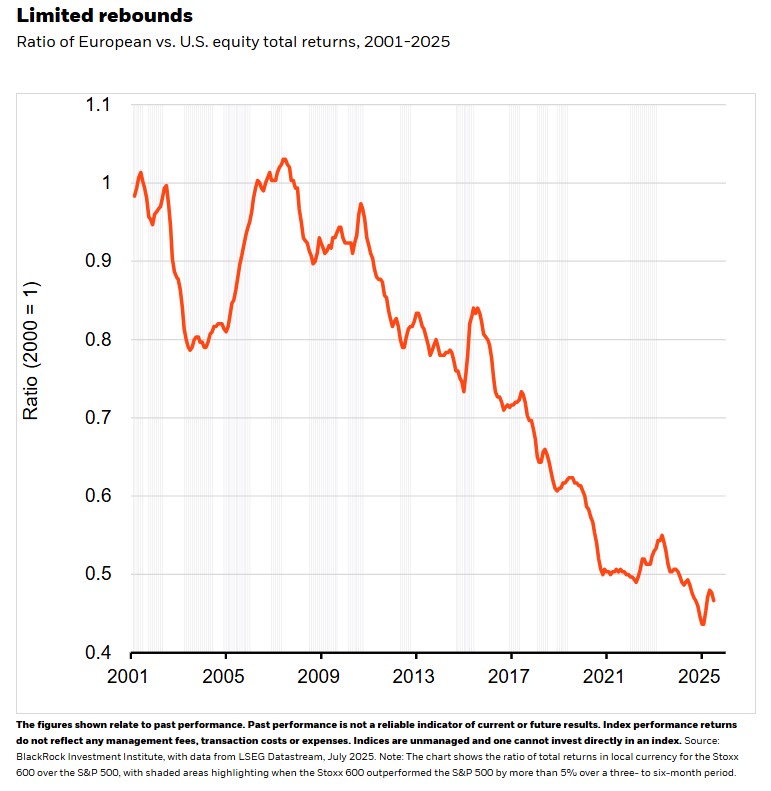

As unusual as this year has seemed, we think it is a more acute manifestation of the profound transformation underway for a few years now. Long-term macro anchors markets have relied on for decades, like stable inflation and fiscal discipline, have weakened. But that does not mean investors should trim risk taking. Mega forces offer a new anchor for returns. And we see immutable economic laws limiting policy shifts and narrowing near-term outcomes: supply chains can’t be rewired overnight and U.S. debt sustainability relies on large foreign funding. So, we’re Investing in the here and now – and putting more weight on our short-term views. We think today’s economic setup still favors U.S. outperformance. European stocks have bested U.S. peers many times since 2000, including early this year, but it’s always faded. See the chart. We think Europe needs to advance its structural reforms to change that.

The recognition that immutable economic laws prevent fast deviation from the status quo allowed us to quickly dial risk back up after the April 2 tariff announcements. And we now see even more cause to stay risk on and overweight U.S. equities. The U.S. is set to enact tax and regulatory reforms that could boost investor sentiment. We see scope for overall corporate earnings to stay solid even if U.S. growth is dented by tariff-induced disruptions and corporate caution.

Getting active across asset classes

In fixed income, by contrast, we prefer euro area government bonds and credit over the U.S. Yields are more attractive in Europe than in the U.S. Yes, long-term U.S. Treasury yields may temporarily fall as markets price in rate cuts amid shifting narratives, but we think sticky inflation will keep the Federal Reserve from cutting far. Plus, high fiscal deficits may prompt investors to seek more term premium, or compensation for the risk of holding long-term U.S. debt. We also prefer local currency emerging market (EM) bonds as the U.S. dollar could weaken more and the EM growth outlook is brighter.

In this volatile environment, we think it is important to carefully manage macro risk: set-and-forget portfolios no longer serve investors well. We find other ways of Taking risk with no macro anchor. They include relative value – or positioning for prices of different securities to converge or diverge – liquidity, regulation and positioning risk. Another way we inform our risk-taking is by Finding anchors in mega forces. We believe they will be durable drivers of returns in both the near and long term.

Across all asset classes, greater dispersion in market and security returns means more opportunity to capture alpha, or above-benchmark returns. Take mega forces as an example. They don’t provide a clear handle on the growth and inflation outlook, unlike macro anchors, and don’t map into broad return drivers. Instead, we need to track their evolution across and within asset classes, get granular with themes and constantly adapt to what’s priced in. Getting active applies across both public and private markets – and we see greater blending of the two within portfolios. Look out for more on just how exceptional this environment is for alpha in coming weeks.

Our bottom line

As long-term macro anchors weaken, we find new ones in mega forces and lean more on our short-term views as immutable economic laws limit the pace of change. We stay overweight U.S. stocks and get active across asset classes.

Market backdrop

U.S. stocks edged up to fresh record highs, with the AI theme taking the lead again. The S&P 500 more than fully recovered from its nearly 15% slide after the April 2 U.S. reciprocal tariffs announcement to end up about 11% in Q2 and up 26% from April lows. U.S. 10-year yields edged up to 4.35% after payrolls increased 147,000 in June, beating expectations. We think that highlights how job creation and wage growth would need to slow much more for inflation to settle at the Fed’s 2% target.

This week, we are monitoring the expiration of the 90-day suspension of U.S. reciprocal tariffs announced on April 2. Negotiators from over a dozen U.S. trading partners are working to finalize an agreement before the deadline. Only the UK and Vietnam have reached a deal so far. Yet an immutable law – supply chains can’t be rewired overnight without serious disruption – means we don’t anticipate tariffs will return to April 2 highs. We watch to see if the pause gets extended.

Week Ahead

July 9 : U.S. tariff pause deadline; China CPI

July 10-17 : China total social financing

BlackRock’s Key risks & Disclaimers:

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of 7th July, 2025 and may change. The information and opinions are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This material may contain ’forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation. Investment involves risk including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are often heightened for investments in emerging/developing markets or smaller capital markets.

Issued by BlackRock Investment Management (UK) Limited, authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from BlackRock Investment Management (UK) Limited. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document is intended for retail clients however, it may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Information Document (KID), which may be obtained from MeDirect Bank (Malta) plc.