Jean Boivin – Head of BlackRock Investment Institute together with Wei Li – Global Chief Investment Strategist, Vivek Paul – Global Head of Portfolio Research and Devan Nathwani – Portfolio Strategist, all forming part of the BlackRock Investment Institute share their insights on global economy, markets and geopolitics. Their views are theirs alone and are not intended to be construed as investment advice.

Key Points

U.S. assets still favored : Moody’s U.S. debt downgrade highlights key challenges. We weigh long-term scenarios but still see U.S. assets playing a core role in global portfolios.

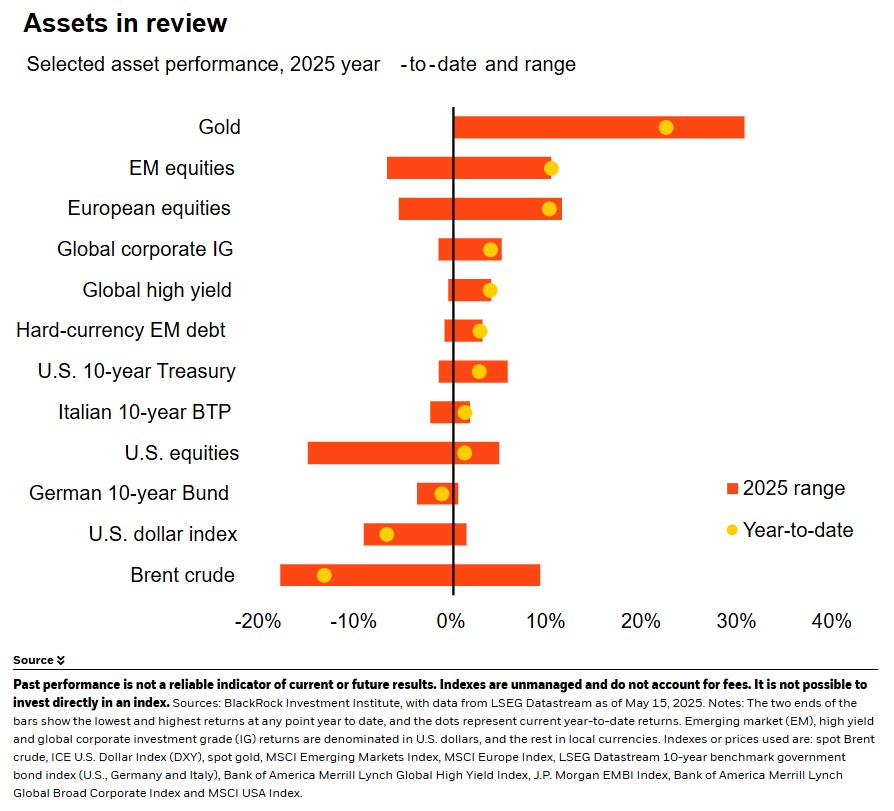

Market backdrop : U.S. stocks rose 2% last week after a tech driven rally, with the S&P 500 up 22% from its April lows. U.S. 10-year Treasury yields ticked up on the week.

Week ahead : This week we watch global flash PMIs for early signs of the business sentiment impact of U.S.-China trade de-escalation. Yet the data will likely remain volatile.

U.S. stocks have soared after sliding with U.S. bonds and the dollar last month. That joint drop stoked talk of U.S. assets losing their long-term appeal. Moody’s U.S. rating cut reinforces our long-held view that investors would want to see a rise in today’s relatively low compensation for the risk of holding long-term U.S. bonds. We still see U.S. assets as core to portfolios. The uncertain outlook means we cannot have conviction in one central scenario alone in our strategic views.

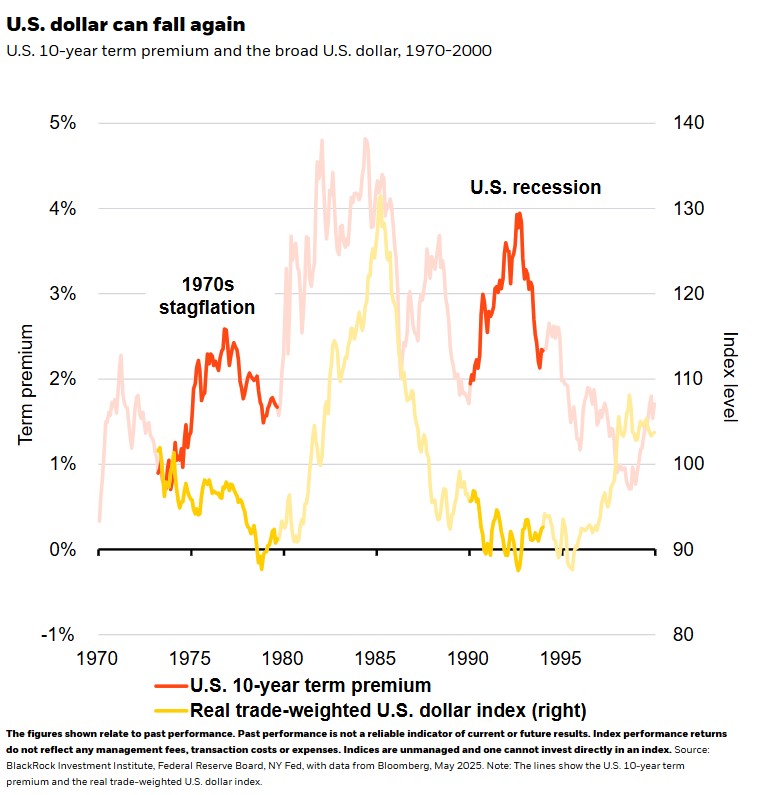

U.S. stocks have jumped 22% from their April lows, according to LSEG data, after the U.S. policy-driven selloff. Tech stocks have led the gains, reinforcing our preference for the artificial intelligence (AI) theme. Yet when equities slid, so did the U.S. dollar and Treasuries – spurring talk of investors losing confidence in U.S. assets. We don’t think that’s the case. The dollar is still historically strong. And we have long argued that investors would want more term premium, or compensation, for holding long-term U.S. bonds given persistently large fiscal deficits, sticky inflation and bond volatility. And long-term Treasuries still carry a relatively low risk premium versus the past. The tariff-driven inflation and quarterly contractions we expect this year are akin to past periods when the dollar fell and term premium rose, and investors didn’t question U.S. assets then. See the chart.

We stay overweight U.S. stocks on a six- to 12-month tactical horizon thanks to U.S. corporate strength and mega forces – big structural shifts like AI that are driving an economic transformation on a par with the industrial revolution. The end state of that transformation is unknowable, making longer-term asset allocation extremely challenging. We can no longer anchor views around a single base case and, as we’ve long argued, static allocations don’t work in the post-pandemic world. That is why we’re developing multiple sets of long-run capital market assumptions for the first time. We build our strategic allocations around a starting point scenario but now formally track others so we know how we would pivot portfolios should they come to fruition. This will allow us to move quickly as we learn more about how the transformation is evolving.

Our strategic starting point

What is our starting point scenario for our strategic views? We believe it has to be the current structure of the global capital market – with U.S. assets still core to portfolios. That’s because hard economic rules limit how quickly the structure can change. The recent 90-day pause on many U.S.-China tariffs illustrates one such rule: Supply chains can’t be rewired quickly without disruption. Moody’s decision to downgrade the U.S. government’s top-notch credit rating last week shines a light on a second rule: keeping U.S. debt sustainable relies on large and steady funding by foreign investors. The downgrade reinforces the U.S. fiscal sustainability challenge that we’ve long flagged, especially persistent U.S. budget deficits at a time when higher interest rates are boosting debt servicing costs. If these dynamics dent the confidence of foreign bond holders, rising term premium could push up bond yields and debt servicing costs even more.

That’s why our starting point also includes our expectation of rising term premium for U.S. Treasuries and persistent inflation pressure. We go overweight inflation-linked bonds and neutral global investment grade credit given wider spreads. We lean into private markets and like infrastructure equity, such as stakes in airports and data centers, as it benefits from mega forces. Private markets are complex and not suitable for all investors. We keep this scenario under review as we learn more.

Our bottom line

Economic transformation makes long-term portfolio construction more challenging. We now use a starting point scenario in our strategic views and formally track others. U.S. assets are still core to portfolios, in our view.

Market backdrop

The S&P 500 rose 2% last week in a tech-led recovery after policy-driven pullbacks in April. That put the index 22% above its April lows. U.S. 10-year Treasury yields ticked up to 4.45%, up more than 50 basis points since early April. Market are pricing in two rate cuts by the Federal Reserve for the rest of the year. U.S. CPI data for April showed easing wage pressures and don’t yet reflect the tariff impact. Yet we think the tight labor market will keep inflation sticky, limiting how much the Fed can cut.

This week, we’re watching global flash PMIs for May for any signs of improvement following the 90-day pause on U.S.-China tariffs. Trade and inflation data from Japan and the UK should shed light on how the U.S. tariff shock is rippling out to the rest of the world.

Week Ahead

May 21 : UK CPI; Japan trade balance

May 22 : Global flash PMIs

May 23 : Japan CPI

BlackRock’s Key risks & Disclaimers:

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of 19th May, 2025 and may change. The information and opinions are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This material may contain ’forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation. Investment involves risk including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are often heightened for investments in emerging/developing markets or smaller capital markets.

Issued by BlackRock Investment Management (UK) Limited, authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from BlackRock Investment Management (UK) Limited. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document is intended for retail clients however, it may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Information Document (KID), which may be obtained from MeDirect Bank (Malta) plc.