Jean Boivin – Head of BlackRock Investment Institute together with Wei Li – Global Chief Investment

Strategist, Natalie Gill – Portfolio Strategist and Beata Gamharter – Senior Investment Strategist, all forming part of the BlackRock Investment Institute share their insights on global economy, markets and geopolitics. Their views are theirs alone and are not intended to be construed as investment advice.

Key Points

Fine-tuning our views

We get selective in artificial intelligence names, moving toward beneficiaries outside the tech sector. We look for quality in bonds after a sharp yield drop.

Market backdrop

U.S. stocks fell last week as recession fears and other factors shook markets. U.S. Treasury yields slid as markets priced in sharp Federal Reserve rate cuts.

Week ahead

The U.S. CPI data this week will show whether services inflation is still cooling. We think the jobs data show market expectations for Fed rate cuts are overdone.

U.S. recession fears and other factors have jolted markets. We could see more volatility flare-ups ahead of the U.S. presidential election. We move from a U.S. tech focus within our equity overweight, leaning further into a wider set of winners from the artificial intelligence (AI) buildout. We don’t see the Federal Reserve cutting policy rates as sharply as markets expect and go underweight U.S. short-dated Treasuries. We prefer medium-term Treasuries and quality credit.

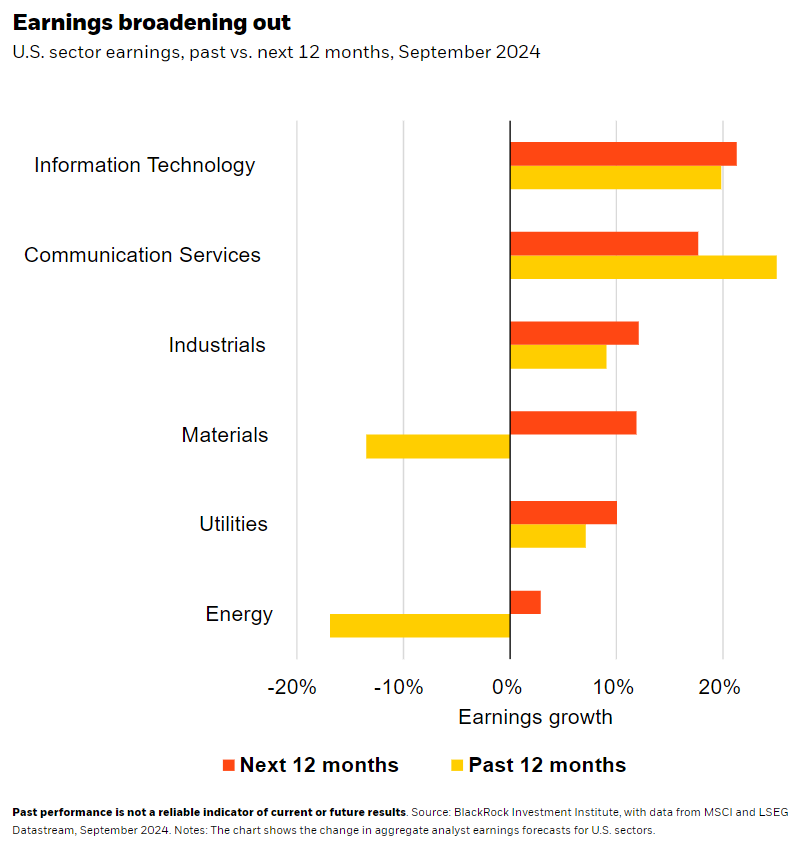

We see multiple factors driving market volatility: resurgent recession fears due to some softer economic data, pre-U.S. election jitters and profit-taking as investors make room for new stock issues. Yet U.S. corporate earnings have proved resilient. All sectors beat expectations for Q2 earnings, driving broad improvement in profit margins. Overall S&P 500 earnings growth was 13% in Q2, beating the 10% consensus expectation, LSEG data shows. Analysts are forecasting broad-based earnings growth over the next 12 months – especially for sectors tied to the AI theme. See the chart. We see a narrowing gap in earnings growth between U.S. tech companies and the rest of the market – even if tech still leads the way – suggesting U.S. equity returns can broaden. We favor high-quality companies delivering consistent earnings growth and free cash flow in case volatility persists.

We still favor the AI theme yet fine-tune our exposure. In the first phase of AI now underway, investors are questioning the magnitude of AI capital spending by major tech companies and whether AI adoption can pick up. While we eye signposts to change our view, we think patience is needed as the AI buildout still has far to go. Yet we believe the sentiment shift against these companies could weigh on valuations. So we turn to first-phase beneficiaries in energy and utilities providing key AI inputs – and real estate and resource companies tied to the buildout. Outside the U.S., we trim our overweight to Japanese equities. The drag on corporate earnings from a stronger yen and some mixed policy signals from the Bank of Japan following hotter-than-expected inflation make us less positive. But we expect corporate reforms to keep improving shareholder returns.

U.S. economy holding up

U.S. earnings growth broadening beyond early AI winners is a sign the economy is more resilient than markets are pricing. Growth is moderating as expected. Yet we view extreme market reactions to softening economic data as overdone. Activity is holding up versus what some sentiment data would imply. The unemployment rate has ticked up due to higher labor supply stemming from an unexpected rise in immigration, not lower demand. In the medium term, we see a shrinking labor force, large U.S. fiscal deficits and mega forces, or structural shifts, like geopolitical fragmentation all underpinning sticky inflation.

Even as inflation is falling toward the Fed’s target in the near term, higher inflation over the medium term will limit how far the Fed can cut rates, we think. Growth jitters and cooling inflation have driven 10-year yields to 15-month lows as investors have priced in more than 100 basis points of cuts by year-end and about 240 basis points of cuts over the next 12 months – implying a Fed response to a recession. That would take policy rates below our view of the neutral interest rate – the rate at which policy neither stimulates nor holds back growth. We go underweight short-dated U.S. Treasuries, looking for income elsewhere in developed markets such as short-dated euro area bonds and credit.

Our bottom line

We expand from a U.S. tech focus, leaning into a wider set of winners from the AI buildout. We trim our Japanese equity overweight. We go underweight U.S. short-dated Treasuries, preferring medium-term maturities and quality credit.

Market backdrop

U.S. stocks tumbled as recession fears and other factors shook markets. The S&P 500 suffered its largest weekly drop in 18 months. Two- and 10-year U.S. Treasury yields slid to around 3.70% as markets priced in sharp Fed rate cuts in the next 12 months. We think these recession fears are overblown, as last week’s U.S. jobs data confirmed. Job growth is slowing but is far from the layoffs that typically signal recession. Wage gains don’t suggest inflation will cool to the Fed’s 2% target, in our view.

In the U.S., August CPI data is the main release this week. Services inflation has fallen in recent months as wage inflation has eased some thanks to a surge in immigration. Whether that labor supply shock persists will influence how much the Fed can cut interest rates, but we think market pricing of cuts is overdone, with wage inflation still too high to be consistent with overall inflation returning to 2%. We, like markets, expect the ECB to cut rates this week.

Week Ahead

Sept. 9: China CPI and PPI

Sept. 11: U.S. CPI

Sept. 12: U.S. PPI; European Central Bank (ECB) policy decision

Sept. 10-17: China total social financing

BlackRock’s Key risks & Disclaimers:

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of 9th September, 2024 and may change. The information and opinions are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This material may contain ’forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation. Investment involves risk including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are often heightened for investments in emerging/developing markets or smaller capital markets.

Issued by BlackRock Investment Management (UK) Limited, authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from BlackRock Investment Management (UK) Limited. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document is intended for retail clients however, it may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Information Document (KID), which may be obtained from MeDirect Bank (Malta) plc.