Wei Li, Global Chief Investment Strategist, Alex Brazier, Deputy Head of the BlackRock Investment Institute, Vivek Paul, Senior Portfolio Strategist and Natalie Gill, Portfolio Strategist all forming part of the BlackRock Investment Institute, share their insights on global economy, markets and geopolitics. Their views are theirs alone and are not intended to be construed as investment advice.

Key Points:

Still stocks over bonds: We recently cut risk, but stick with stocks over bonds for now. Equity prices now reflect much of the worsening macro outlook and hawkish Fed, in our view.

Market backdrop: Markets came to grips last week with the trade-off central banks face: choke off growth or live with inflation. Yields fell and stocks bounced off new 2022 lows.

Week ahead: U.S. retail sales and other activity data will give investors a read on growth momentum. We believe the restart from pandemic lockdowns has room to run.

Equities have fallen hard this year on the prospect of rapid rate increases to rein in inflation, the tragic Ukraine war and a slowdown in China. We recently reduced risk, yet keep our modest stocks overweight. Why? The selloff means more of these risks are now priced. We also believe the Fed’s sum total of rate hikes will be historically low and see recession fears as overblown. We think equities remain more attractive than bonds, even as the historic sell-off in bonds has cut the gap between the two.

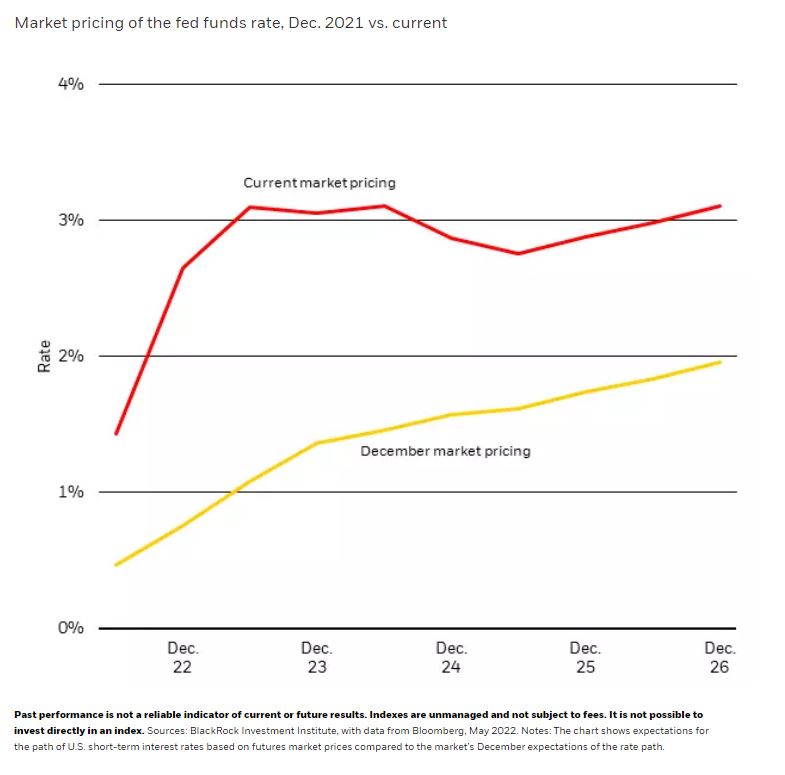

Caution: steep rate path ahead

We started the year with an overweight in equities and underweight in bonds. The macro outlook has worsened since then. The Ukraine war added to already high inflation stemming from pandemic-related supply constraints. The Fed started to talk tough on inflation, and the market has quickly priced in a series of steep rate rises (the red line in the chart), whereas it was still expecting a shallow trajectory in December (the yellow line). And we now see a rising risk the Fed will raise policy rates to a level that slows the economy. The latest: Growth in China has slowed amid widespread Covid lockdowns. Both stocks and bonds have sold off in the face of these mounting challenges. We stick with our equities overweight for now. Why? First, much of the risks to growth are now reflected in stock prices, we believe, keeping valuations attractive. Second, we still think the cumulative total of Fed rate hikes will be historically low, given the level of inflation. We see the Fed ultimately choosing to live with core inflation that’s a bit higher than its 2% target, rather than fight it because of the costs to growth and jobs.

The worsening economic outlook has prompted us to reduce portfolio risk this year. We downgraded European equities in March on the energy shock. We followed with a downgrade of Asian assets last week, coupled with an upgrade of investment grade credit and European government bonds. The sell-off in the bond market has narrowed the gap between the stocks and bonds, in our view, and created pockets of value. We still see longer-term yields rising further as investors demand a higher term premium, or compensation for the risk of holding government bonds amid high inflation and debt loads. As a result, we are not changing our overall bonds underweight and maintain our relative preference for equities.

Reducing risk

What are the risks? Today’s inflation is very different from the past 30 years, and central banks need a new playbook. Inflation is always caused by excess demand over a certain amount of supply. That doesn’t mean excessive demand is driving inflation, as has been mostly the case since the 1990s. The real question: Is demand unusually high or is supply abnormally low? We think it’s the latter. The economy is working its way through two major shocks: the pandemic and the war in Ukraine. This has created supply constraints such as a tight labor market (caused by the “Great resignation”) that will take time to resolve. Why does all of this matter? If inflation is caused by supply factors, the Fed faces a stark choice: choke off growth with higher rates – the old playbook – or live with more persistent inflation. The risk is that the Fed fails to recognize the trade-off and pushes rates to such levels they destroy growth and jobs.

Markets are waking up to the risks surrounding this trade-off, and now look to be pricing in a fed funds rate of close to 3.5% in the very long run. If that’s true, equities may have more room to fall: Higher discount rates make future cash flows less attractive. We think the Fed ultimately won’t go this high for fear of hurting growth, but recognize hawkish policy pronouncements can lead markets to believe differently. This is why we brace for more volatility in the short run – and why we are not adding to our equities overweight despite improved valuations.

Our bottom line

We stay overweight equities and underweight bonds, but have reduced risk to reflect the worsening macro outlook. The momentum of the restart of economic activity is still strong, especially in the U.S., so we don’t see a recession ahead. We prefer developed market stocks, especially U.S. and Japanese equities. We particularly like the U.S. market’s quality bent featuring companies with strong cashflows and balance sheets. We would turn more negative on equities should the risk of the Fed slamming the brakes on the economy materialize and trigger a material slowdown.

Market backdrop

Markets are coming to grips with the stark growth-inflation trade-off central banks are facing to rein in supply-driven inflation: choke off growth or live with higher inflation. Last week, markets started to price in the risk that the Fed will push ahead with the first option. Yields on 10-year U.S. Treasuries fell, and stocks bounced off new 2022 lows. We believe the sharp trade-off will ultimately give the Fed pause before taking rates up to levels that trigger a material slowdown.

U.S. activity data and surveys will shed light on the ongoing restart of economic activity and the shift in consumer spending back to services, from goods. Market concerns around a pronounced slowdown in the U.S. miss the key point that the restart has further room to play out, in our view.

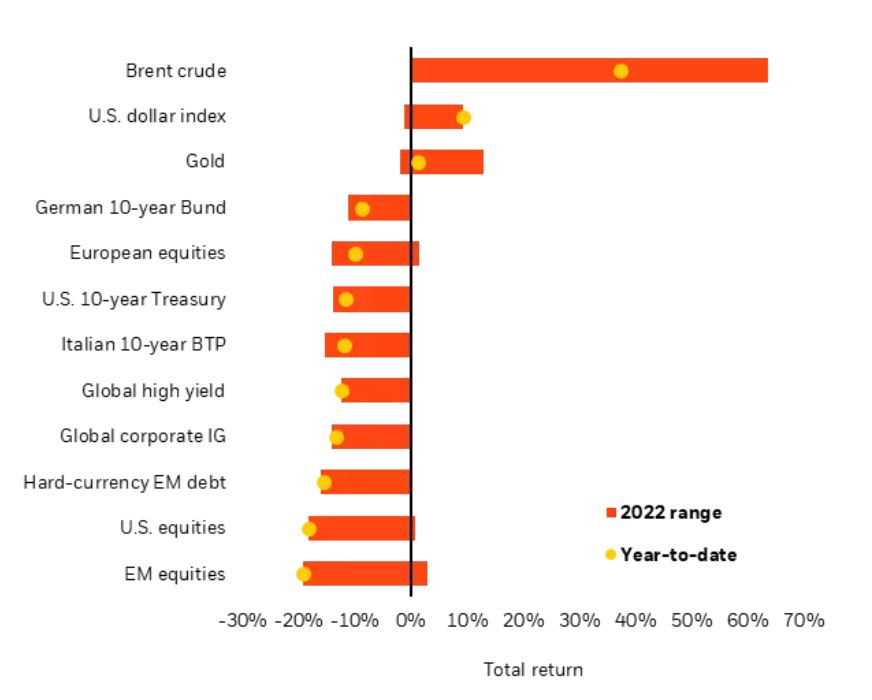

Past performance is not a reliable indicator of current or future results. Indexes are unmanaged and do not account for fees. It is not possible to invest directly in an index. Sources: BlackRock Investment Institute, with data from Refinitiv Datastream as of May 12, 2022. Notes: The two ends of the bars show the lowest and highest returns at any point this year to date, and the dots represent current year-to-date returns. Emerging market (EM), high yield and global corporate investment grade (IG) returns are denominated in U.S. dollars, and the rest in local currencies. Indexes or prices used are: spot Brent crude, ICE U.S. Dollar Index (DXY), spot gold, MSCI Emerging Markets Index, MSCI Europe Index, Refinitiv Datastream 10-year benchmark government bond index (U.S., Germany and Italy), Bank of America Merrill Lynch Global High Yield Index, J.P. Morgan EMBI Index, Bank of America Merrill Lynch Global Broad Corporate Index and MSCI USA Index.

Week Ahead

- May 17: U.S. retail sales and industrial production; Japan GDP

- May 18: UK CPI; Japan trade data

- May 19: U.S. Philly Fed Business Index; Japan CPI; UK retail sales

BlackRock’s Key risks & Disclaimers:

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of April 25th, 2022 and may change. The information and opinions are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This material may contain ’forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation. Investment involves risk including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are often heightened for investments in emerging/developing markets or smaller capital markets.

Issued by BlackRock Investment Management (UK) Limited, authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from BlackRock Investment Management (UK) Limited. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Investor Information Document (KIID), which may be obtained from MeDirect Bank (Malta) plc.