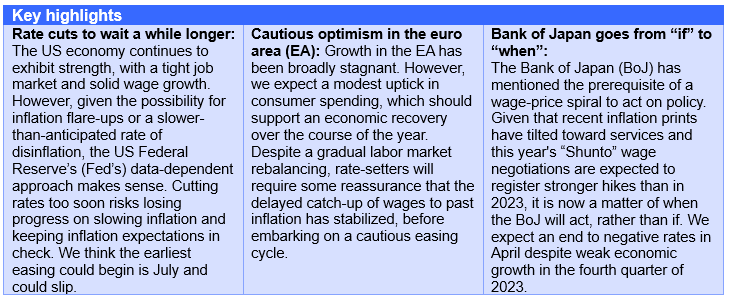

Franklin Templeton Fixed Income economists are seeing evidence of sticky inflation across the Group of Three (G3) nations. While central banks in the United States and eurozone are gauging when to embark on monetary easing, the Bank of Japan will likely hike in April. All three will continue to monitor wages (and their impact on services inflation) and the balance of risks to economic growth.

Executive Summary

US economic review

US economy: A flashback to the 1990s soft landing

- The US economy continues to exhibit signs of strength. Although household spending slowed through 2023, year-over-year (y/y) growth rates remained at their longer-term averages. A still-robust labor market, solid wage and real disposable income growth, along with strong household balance sheets, should remain supportive of consumption going forward, albeit slower than in 2023 owing to a significantly smaller savings cushion.

- While labor demand has slowed due to a decline in job openings, payroll growth continues to oscillate around its longer-term average. Excess demand for labor, at 2.8 million, is still about 1.5 million above pre-pandemic levels. However, the slowdown in labor-force participation may worry the Fed in terms of the upward pressure this could put on wages.

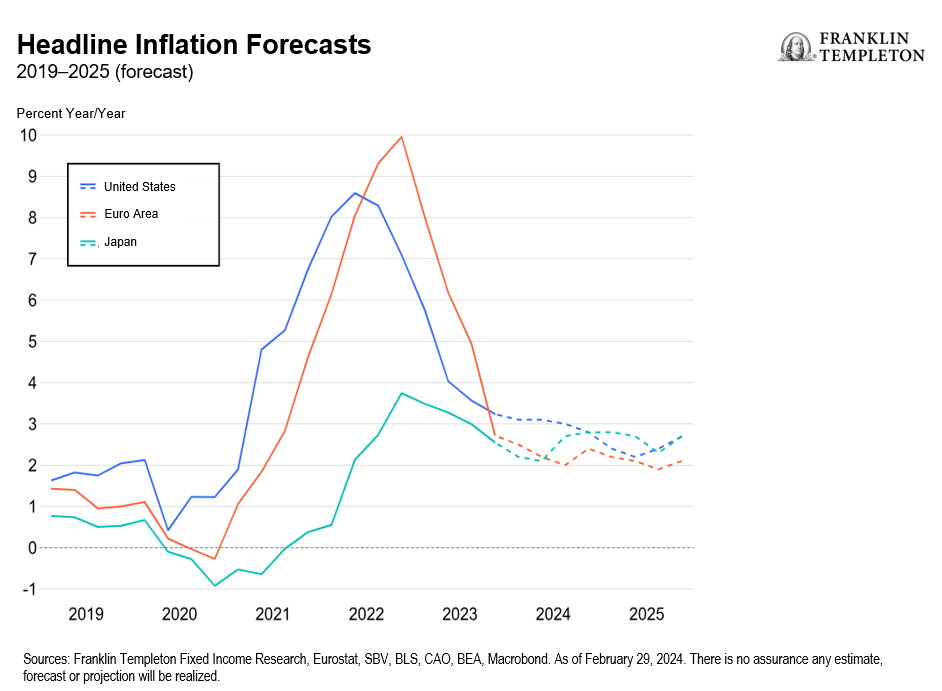

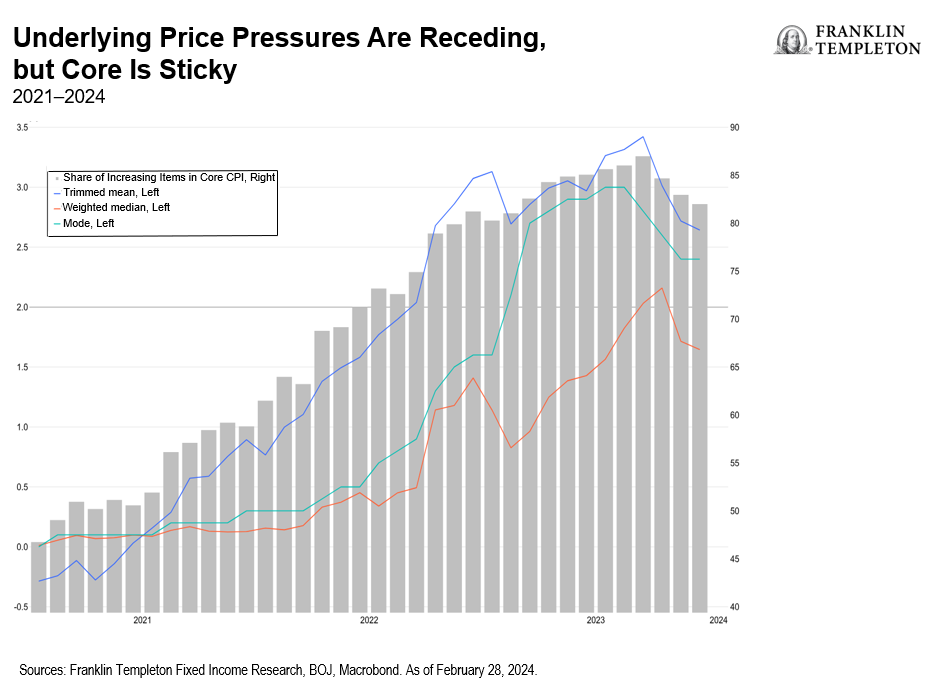

- The January inflation prints serve as a reminder that the potential for inflation flare-ups remains. Equally concerning is the rise in the prices-paid measures for both the manufacturing and services components of the Institute of Supply Management report. Small businesses have also increasingly considered price hikes and wage increases. Therefore, we think the Fed can hold interest rates high for a while longer to ensure inflation is sustainably making its way down to 2%.

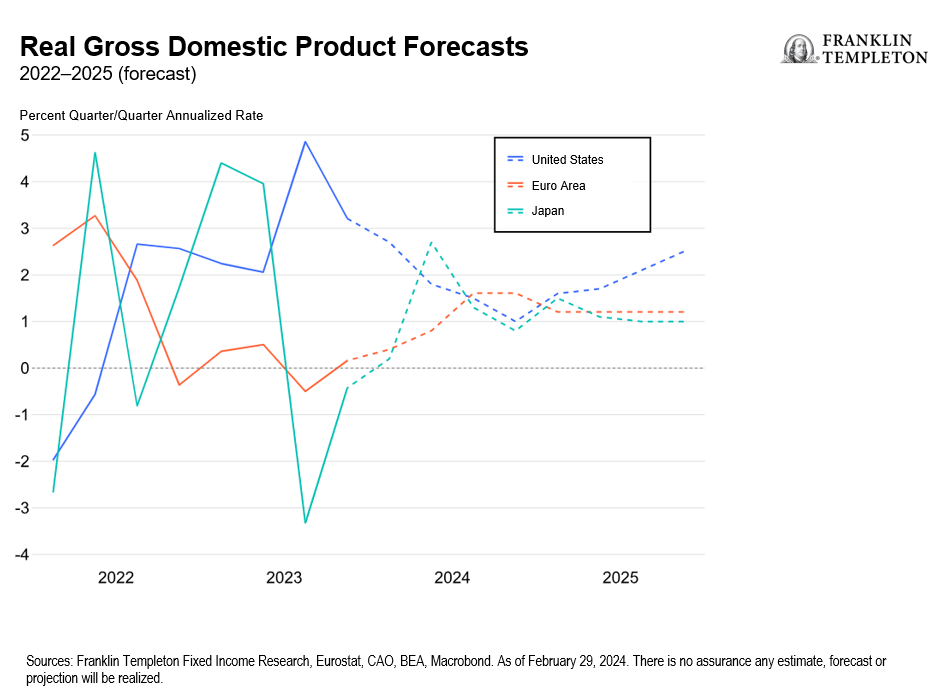

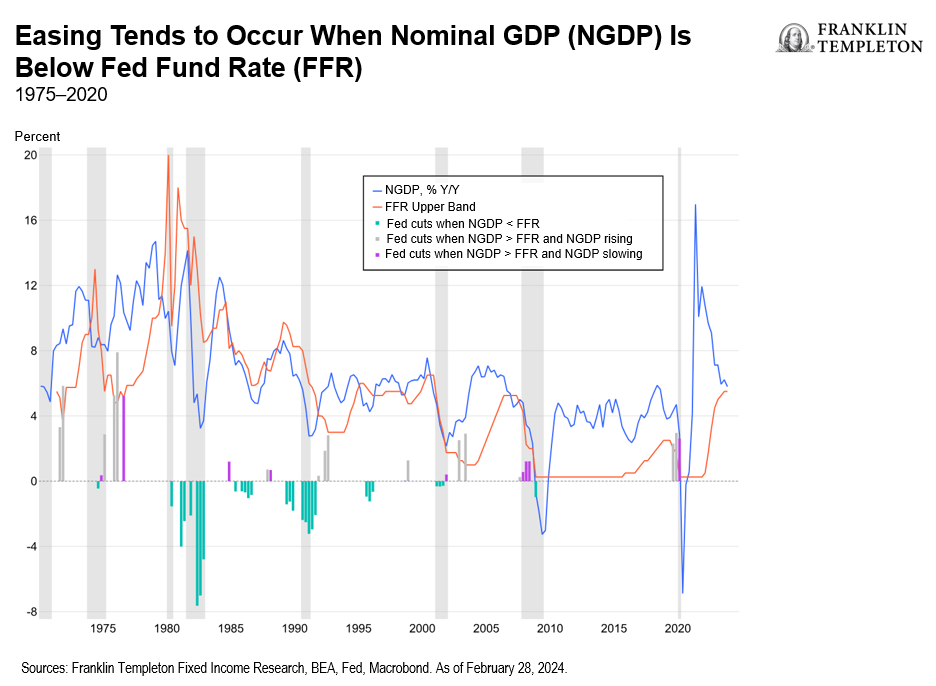

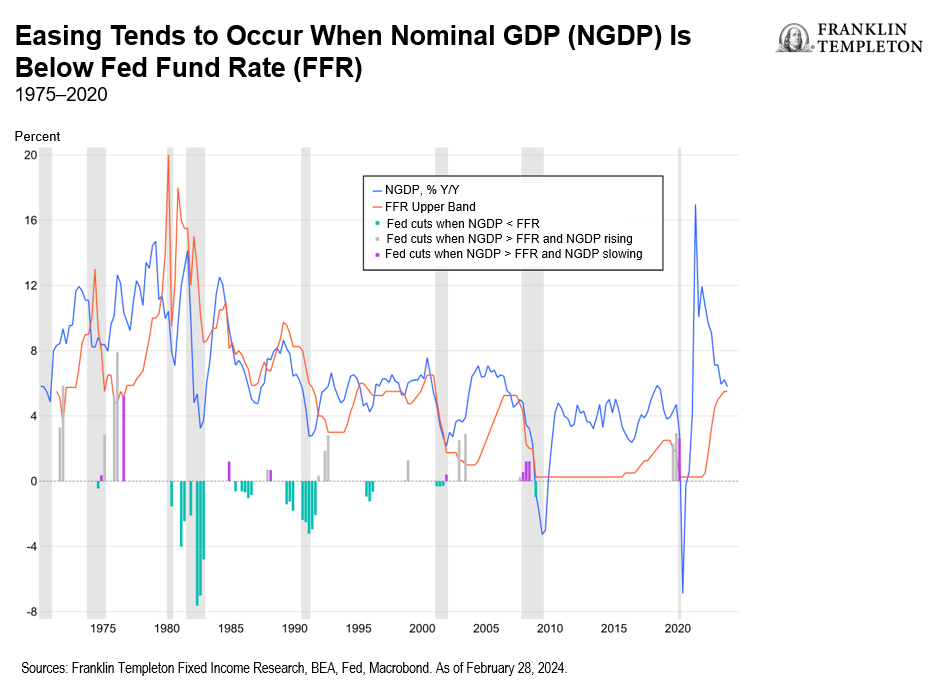

- First Fed rate cut most likely postponed until July at the earliest, in our view. Most easing cycles since the Volcker-led Fed have started with y/y nominal gross domestic product (GDP) growth below the level of the funds rate—as Bloomberg columnist Cameron Crise noted. The 1995 cycle implies easing may not start before September, which seems like a reasonable possibility as markets too have currently assigned the highest probability for a first rate cut in September. However, nominal growth will likely slip below the policy rate by the second quarter, leaving July as a possibility for a rate cut, in our view. Real rates will also likely be pushing above 3% by then.

- How deep the Fed cuts in the coming easing cycle will depend on the nature of the economic “landing.” Productivity growth, and in effect, the Fed’s view of the real neutral rate (R*) are important determiners of forward policy. A rerun of the mid-1990s—a situation where productivity growth does indeed take off (nascent signs of that occurring), which would also imply a higher R*—could make expectations of 150-200 basis points of rate cuts over the next couple of years seem excessive.

- The economy is showing timid signs of improvement. Eurozone growth was stagnant over the fourth quarter of 2023 (Q4), supported by upside surprises in Spain and Italy, while France sidelined and Germany recorded a contraction. We expect a gradual, consumption-driven recovery throughout the first half 2024.

- Private consumption is fragile, but on the mend. Consumer confidence remains subdued, as economic uncertainty weighs on spending intentions. Going forward, a still-strong labor market, robust wage growth and declining inflation should support real incomes and a consumption recovery.

- The job market is resilient and undergoing a gradual rebalancing. Employment growth continued to outpace GDP growth in Q4, with the unemployment rate remaining at historic lows. The labor market is now witnessing a gradual cyclical rebalancing. Hiring is likely to slow in the quarters ahead, which is symptomatic of high employment and rising labor costs. This should help stabilize wages.

- The credit drag on the economy has likely peaked and will diminish going forward. Credit conditions have stabilized, and credit flows should pick up from the very weak levels witnessed in the previous quarters. It is clear to us that the monetary policy transmission mechanism has worked, and its reversal will ease the compression in investments. However, the timing of this remains uncertain.

- Sustainable deflation is dependent on an uncertain wage and productivity outlook. Easing energy and goods prices have mostly supported the decline in headline inflation. Meanwhile, services inflation has proved sticky, supported by salary increases. Rising wages and declining labor productivity will likely continue to put upward pressure on unit labor costs.

- The European Central Bank (ECB) is likely to proceed with caution. The focus will remain on second-round effects, especially on historically high wage inflation, firms’ profit margins and weak productivity. Policymakers will likely seek reassurance of wage growth stabilization before embarking on monetary policy easing and will proceed cautiously in 2024.

- Growth has been sluggish with a technical recession in Q4. The first quarter of 2024 will likely continue to be on weak footing, owing to repercussions from the Noto earthquake and auto production disruptions. But the outlook is not completely bleak. We expect a modest recovery in the second half of 2024 as stronger wage gains cushion private consumption, and private capital expenditure (capex) looks to enhance productivity and digitization. We project GDP to grow at 0.5% y/y in 2024, but then bounce back to 1.2% in 2025, well above potential growth.

- Inflation has been moderating, thanks largely to goods-price disinflation. But service prices are turning sticky. There are plaguing labor shortages in Japan, and wage gains are likely to strengthen in this year’s “Shunto” negotiations. Given that firms are still passing higher costs to other firms, and in turn to customers (the services component of the Producer Price Index remains elevated at 2.1% y/y, and firms from insurance to delivery partners are reportedly raising costs), we think it would be unwise to take the current bout of disinflation at face value. Inflation has slowed, but prices could be stickier around the 2% handle.

- Our attention thus turns to the options in front of the BoJ. Recent commentary has aligned toward possible action if sufficient evidence of a wage-price spiral emerge. This is already in the works, and with the upcoming wage negotiation data expected to be stronger than last year’s, we believe the BoJ will overlook the current damp growth prospects to end the yield curve control framework and exit negative interest-rate policy by April. A weak recovery will underline more cautious tightening trajectory, although we do not expect aggressive rate hikes just yet.

- Higher inflation structurally justifies higher nominal rates, however, real rates in Japan have been steeped in the negative. This has in turn helped to support growth. So, the BoJ’s balance here is crucial—any rate hikes will push up real rates, possibly leading to further weakness. We therefore expect substantial policy tightening only later in the year, once the recovery makes some headway. We expect sufficient forward guidance to underline any pullback in Japanese government bond purchases in the coming months.

Franklin Templeton Key risks & Disclaimers:

What Are the Risks?

All investments involve risks, including possible loss of principal.

Fixed income securities involve interest rate, credit, inflation and reinvestment risks, and possible loss of principal. As interest rates rise, the value of fixed income securities falls.

Green bonds may not result in direct environmental benefits, and the issuer may not use proceeds as intended or to appropriate new or additional projects.

The managers’ environmental, social and governance (ESG) strategies may limit the types and number of investments available and, as a result, may forgo favorable market opportunities or underperform strategies that are not subject to such criteria. There is no guarantee that the strategy’s ESG directives will be successful or will result in better performance.

Any companies and/or case studies referenced herein are used solely for illustrative purposes; any investment may or may not be currently held by any portfolio advised by Franklin Templeton. The information provided is not a recommendation or individual investment advice for any particular security, strategy, or investment product and is not an indication of the trading intent of any Franklin Templeton managed portfolio.

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Issued by Franklin Templeton Investment Management Limited (FTIML) Registered office: Cannon Place, 78 Cannon Street, London EC4N 6HL. FTIML is authorised and regulated by the Financial Conduct Authority.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from Franklin Templeton Investment Management Limited (FTIML). No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Information Document (KID), which may be obtained from MeDirect Bank (Malta) plc.

{kind=link}