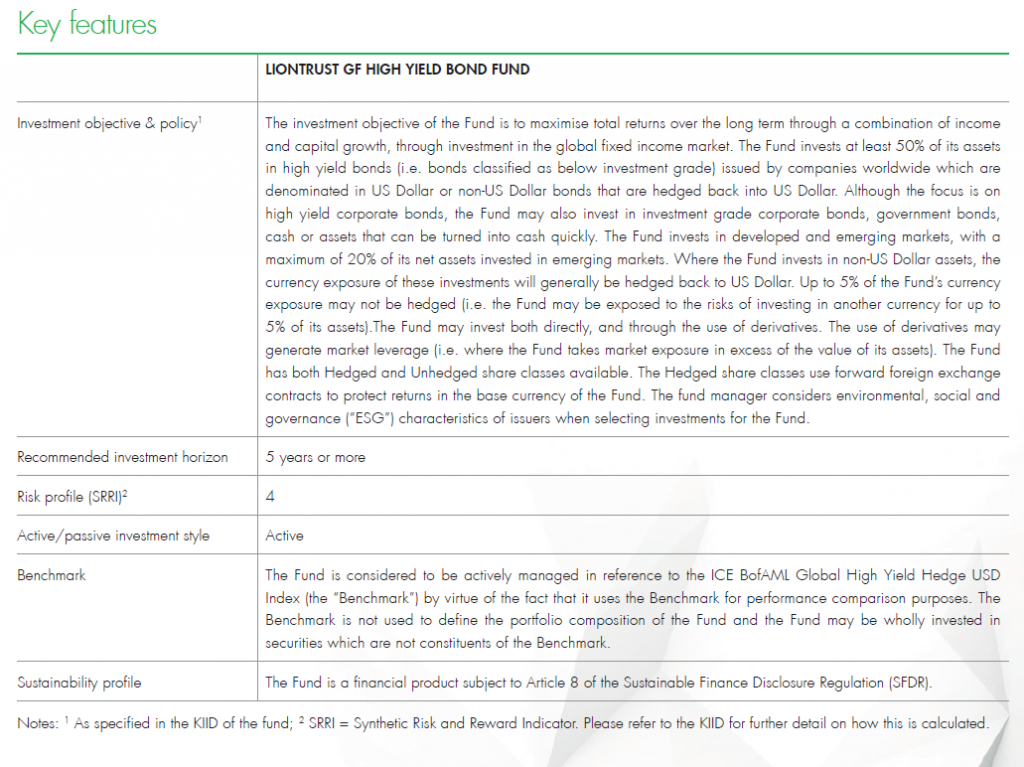

Liontrust GF High Yield Bond Fund is manufactured by Liontrust Fund Partners LLP and represented in Malta by MeDirect Bank (Malta) plc.

Market review

The global high yield market returned of 3.3% in US dollar terms in Q1 2023. US high yield market returned 3.7% while the European market returned 3.3%. Both markets performed well despite the market volatility around the collapse of SVB and the Credit Suisse/UBS merger in March. These events raised concerns around the banking sector, giving an indication as to whether the monetary policy actions in the US were working and therefore resulting in some companies failing to battle the higher interest rate environment.

Performance was also supported by the stall in primary market issuance, with issuers shelving deals until a more suitable market environment presents itself. The high yield market doesn’t have a looming maturity wall to address as many issuers have refinanced and will only start to have more meaningful debt maturities to address from 2025 onwards. Corporate earnings were on the whole good and default rates are rising but from a very low level. The US and European high yield markets saw ratings decompression, where CCC bonds outperformed BB and B bonds in January and February, before it switched and better-quality bonds outperformed CCC bonds in March.

When hedging via interest rate futures, we took the opportunity to hedge some of the natural, albeit low, level of duration that exists in high yield bonds, using. When yields moved higher, these were closed out.

Fund review

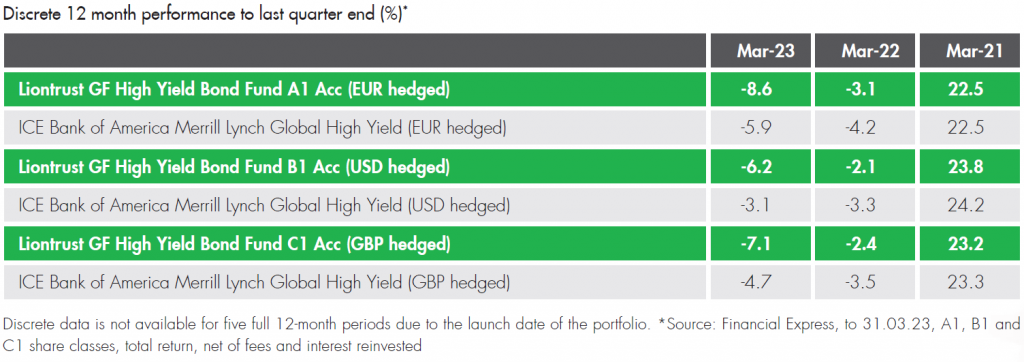

Over the quarter, the Liontrust GF High Yield Bond Fund (A1, accumulation class, total return in euros) produced a return of 2.7% versus the ICE BAML Global High Yield index’s (euro hedged) 2.7%*.

Relative to index, the best performing sectors in the Fund in Q1 2023 were capital goods, telecommunications, healthcare and basic industry. Strong contributors to stock picking include Ardagh (a packaging company), VirginMedia, Profine (a PVC window frame manufacturer), and two healthcare names, Cheplapharm and Catalent. The Catalent bonds were marked seven points up on the back of rumours that it is an acquisition target for Danaher (an investment grade rated company).

Areas where our relative underweight position was a drag to performance were in more cyclical sectors, such as energy and leisure. This shouldn’t come as a surprise as the Fund has a bias towards less cyclical defensive credits.

During the quarter the Fund participated in four new issues, one of which was Sealed Air. Sealed Air is a leading global provider of packaging solutions integrating high-performance materials, automation, equipment and services. The company is well diversified both geographically and with its customer base. Financial performance has been good and it has clearly demonstrated its ability to acquire and integrate businesses in order to expand successfully. The US dollar-denominated bonds are rated Ba2/BB+ and were priced attractively below par with a 6.875% coupon.

We participated in a euro perpetual new issue from Swiss bank Julius Baer. The bond was rated Baa3 with a 6.625% yield, which we believe was attractive for the structure given the defensiveness of the underlying business. The aftermath of the complete write-down of Credit Suisse AT1 led to the underperformance of this bond, which was one of the drags in the quarter, alongside Barclays AT1. Elsewhere, although the real estate sector has been less dramatic than last year, stock selection was mixed in the quarter. The Fund had a positive contribution from Castellum and Peach, with both companies raising equity, though CPI Property continues to be a drag despite the fact its operational performance has been good.

We participated in a new issue from existing holding TransDigm, a manufacturer of engineered aerospace components for commercial airlines, aircraft maintenance facilities, original equipment manufacturers and various agencies of the US government. We particularly like the strong margins of the business and positive free cash flow generation. The new issue is higher up the capital structure; a US dollar-denominated bond rated Ba3/B+ with a 6.75% coupon.

Azelis is the most recent deal we participated in. It is a leading global distributor of specialty chemicals and food ingredients. Azelis operates in more than 50 countries and has a presence in more than 40 industry sectors. It has a resilient business, growth opportunities both organically and through M&A, as well as market leading positions in highly fragmented markets. Its financial performance has also been good. The bonds are euro-denominated, rated BB+ and came with a coupon of 5.75%.

Outlook

The global high yield market benefitted from a strong rally at the beginning of the year before experiencing some volatility towards the end of the quarter. Risks such as the collapse of SVB and the Credit Suisse/UBS merger are typically more likely to emerge in an environment where rates are higher and funding conditions tighter. In the Credit Suisse situation where its AT1 debt was written off, investor sentiment of the sub-asset class has taken a turn. Concerns were raised around the language behind AT1 debt in general and how they would be treated if a bank got into trouble. Since the wobble, we have seen the retracement of AT1 debt and believe that investors are convinced that the recent volatility experienced is down to idiosyncratic elements rather than a banking crisis or the beginning of a domino effect of failing companies sparked by the Fed’s monetary policy tightening cycle. These fears of broader contagion from the banking turmoil have been alleviated by governments and central banks.

In the Fund, we have around 3% AT1 exposure and are comfortable with the credits we have exposure to. Some have been marked down purely because of contagion, but we believe the bonds will perform well over time. As the sub-asset class has the potential to be volatile, we are limiting our overall exposure. Primary issuance has been minimal during the last quarter, and the issuers that have come to market are predominantly using funds for general corporate purposes rather than to finance M&A activity; they have also typically been from higher rated credits. We have yet to see lower quality credits come to market, which is in part an indication of the market environment but also a reflection of investors’ appetite for higher quality credits. The deals that have come to market have been oversubscribed, demonstrating that there is demand for new issues but at a price. This strong technical around lack of issuance in the asset class has also helped the positive performance of the asset class year-to-date.

With default rates still low, corporate fundamentals are generally looking resilient with no immediate debt maturity wall to address. We believe our bias towards better quality, less cyclical credits should be beneficial in this market environment. However, we are mindful of the potential mild recessionary period in the latter part of the year, and feel we have invested in credits that are well positioned to deal with such a headwind. The Fund is currently offering yield of almost 10% for sterling-based investors, which we view this as an attractive entry point for investors.

Liontrust Key risks & Disclaimers:

Past performance is not a guide to future performance. Do remember that the value of an investment and the income generated from them can fall as well as rise and is not guaranteed, therefore, you may not get back the amount originally invested and potentially risk total loss of capital.

The issue of units/shares in Liontrust Funds may be subject to an initial charge, which will have an impact on the realisable value of the investment, particularly in the short term. Investments should always be considered as long term.

Investment in the GF High Yield Bond Fund involves foreign currencies and may be subject to fluctuations in value due to movements in exchange rates. The value of fixed income securities will fall if the issuer is unable to repay its debt or has its credit rating reduced. Generally, the higher the perceived credit risk of the issuer, the higher the rate of interest. Bond markets may be subject to reduced liquidity. The Fund may invest in emerging markets/soft currencies and in financial derivative instruments, both of which may have the effect of increasing volatility. The Fund may invest in derivatives. The use of derivatives may create leverage or gearing. A relatively small movement in the value of a derivative’s underlying investment may have a larger impact, positive or negative, on the value of a fund than if the underlying investment was held instead.

Issued by Liontrust Fund Partners LLP (2 Savoy Court, London WC2R 0EZ), authorised and regulated in the UK by the Financial Conduct Authority (FRN 518165) to undertake regulated investment business.

This document should not be construed as advice for investment in any product or security mentioned, an offer to buy or sell units/shares of Funds mentioned, or a solicitation to purchase securities in any company or investment product. Examples of stocks are provided for general information only to demonstrate our investment philosophy. It contains information and analysis that is believed to be accurate at the time of publication, but is subject to change without notice. Whilst care has been taken in compiling the content of this document, no representation or warranty, express or implied, is made by Liontrust as to its accuracy or completeness, including for external sources (which may have been used) which have not been verified. It should not be copied, faxed, reproduced, divulged or distributed, in whole or in part, without the express written consent of Liontrust. Always research your own investments and (if you are not a professional or a financial adviser) consult suitability with a regulated financial adviser before investing.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from Liontrust Fund Partners LLP. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest should always be based upon the details contained in the Prospectus and Key Information Document (KID), which may be obtained from MeDirect Bank (Malta) plc.