Franklin Mutual Series’ Investment Strategist Katrina Dudley believes that higher inflation in Europe stemming from rising energy prices, as well as lower relative interest rates, may keep the euro under pressure.

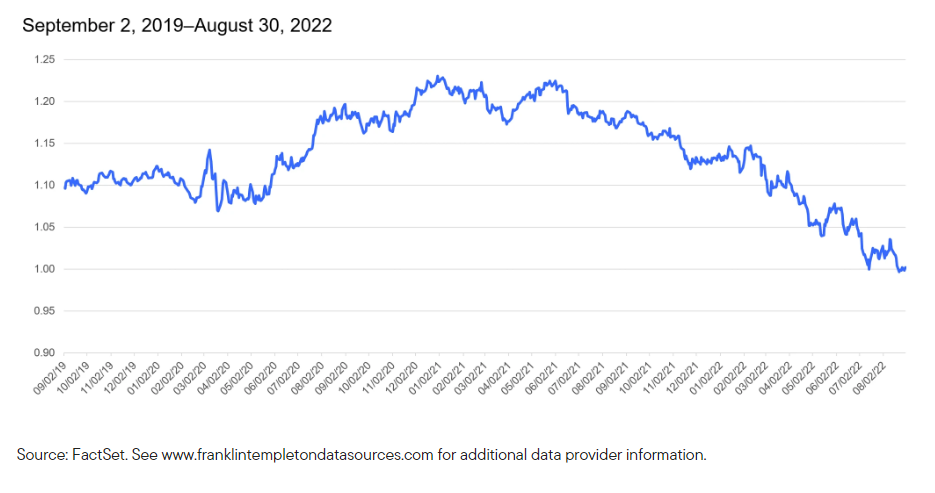

The euro has reached parity with the US dollar. The war in Ukraine, a resulting spike in energy prices and a central bank that has been slower than the US Federal Reserve (Fed) to hike interest rates to tame inflation has sent the euro tumbling against the US dollar over the first eight months of 2022. A fast recovery for the currency may be some ways off, but the euro’s depreciation could create near-term opportunities for value stock investors.

Energy spikes

While the euro was declining gradually against the US dollar at the start of the year, Russia’s invasion of Ukraine sparked a more aggressive selloff. The potential for a sharp pickup in inflationary pressures and the region’s lack of energy and defense security were largely to blame.

The Euro Drops Against the US Dollar in 2022

Euro/US Dollar

In the wake of the invasion, energy prices across the region surged amid fears of natural gas export disruptions from Russia that have come to fruition. We have seen the Russians recently shut down the important Nord Stream pipeline, first for maintenance and now until sanctions are lifted. The move comes at a time when countries like Germany are filling their natural gas reserves to ensure they have enough gas to get through the winter.

Over time, we expect Germany and other European countries that have depended on Russian gas to transition to other energy sources, such as renewables and liquified natural gas (LNG). But over the near term, we could see ongoing supply challenges and continuing high energy prices.

The energy supply disruptions also come at a time when other inflationary pressures were already biting across the continent from disrupted supply chains. Moreover, low rivers in Europe this summer have made shipping more costly and more challenging.

Like the United States, Europe is grappling with unprecedented levels of inflation. The region’s annual consumer price index rose 8.9% in July, up from 8.6% in June, and 2.2% a year earlier, according to data from European statistics agency Eurostat. In both regions, these rising costs are eating away at consumers’ purchasing power and negatively impact domestically oriented consumer businesses.

Our research has shown that inflation has a significant impact on relative currency levels. Should high energy prices and other inflationary pressures remain stickier in Europe than the United States, we could see a further erosion of the euro’s value over the coming months.

The rate differential grows

The European Central Bank (ECB) and the US Fed have raised interest rates at different speeds in the wake of these inflationary pressures. This differential is further exacerbating the weakness in the euro. Generally, higher interest rates increase the value of a country’s currency as the higher rates tend to attract more foreign investment.

The ECB in contrast lifted its key interest rates by 125 basis points so far in 2022, with more hikes are expected over the remainder of 2022. Like the United States, the central bank is focused on curbing inflation, and it too is balancing the need for price stability against slowing economic growth. The war and its knock-on effects have put unprecedented stresses on the European economy that we believe will take time to ease and have the potential to tip the region into recession.

Growth stalls

A falling euro has had a mixed impact on European economic activity. US travelers have been flocking to Europe, which has been positive for growth in those countries, particularly in Southern Europe, that were hit particularly hard due to COVID-19. These tourists are finding that their dollar buys much more than it did a year earlier, bolstering local economic activity.

But for European consumers, the cost of imports, particularly denominated in US dollars, like commodities, is rising with the decline in the euro. The weaker European economy also means that companies will have more difficulty in passing along higher costs to consumers and end-users.

The depreciation of the euro, inflation pressures, fears of a European recession and pressures on consumers impact each company differently. Here, we believe active stock selection will be crucial. Investors will need to understand the extent to which a company is naturally hedged and if there are cost and revenue mismatches that could result in either an earnings benefit or a decline.

Overall, we have seen European equity markets trade at a sizable discount to their US counterparts over the past few years, given the heavier weightings toward more value-oriented sectors such as financials, energy and materials. We have seen some areas of the market come roaring back as value returned to favor this year. A weakening euro creates both challenges and opportunities for European companies. Knowing where to look, and what to look for, will be critical in the months ahead.

Franklin Templeton Disclaimer:

Important legal Notice

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Distributors, LLC, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com – Franklin Distributors, LLC, member FINRA/SIPC, is the principal distributor of Franklin Templeton U.S. registered products, which are not FDIC insured; may lose value; and are not bank guaranteed and are available only in jurisdictions where an offer or solicitation of such products is permitted under applicable laws and regulation.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal. The value of investments can go down as well as up, and investors may not get back the full amount invested. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions. Investments in foreign securities involve special risks including currency fluctuations, economic instability and political developments. Value securities may not increase in price as anticipated or may decline further in value.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from Franklin Templeton Investment Management Limited (FTIML). No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Investor Information Document (KIID), which may be obtained from MeDirect Bank (Malta) plc.