Wei Li, Global Chief Investment Strategist, together with Alex Brazier, Deputy Head, Scott Thiel, Chief Fixed Income Strategist, and Ann-Katrin Petersen, Senior Investment Strategist all forming part of the BlackRock Investment Institute, share their insights on global economy, markets and geopolitics. Their views are theirs alone and are not intended to be construed as investment advice.

Key Points:

Challenges ahead: Europe is facing the risk of an energy shock-driven recession and periphery stress. That’s why we think the ECB will stop hiking earlier than the Fed.

Market backdrop: Relentless U.S. inflation last week signaled a big rate hike by the Fed later this month. Long-term yields fell amid fears rate hikes may trigger a slowdown.

Week ahead: We see the ECB raising rates by 0.25% this week amid high inflation and despite recession fears. We also expect details on its anti-fragmentation tool.

The European Central Bank (ECB) is set to lift rates for the first time in over a decade this week. Both the ECB and Fed are for now pandering to “the politics of inflation,” or pressure to tame inflation. We think the ECB will pause its hiking first. Why? The energy crisis means Europe’s growth is likely to stall soon. Higher rates and political turmoil may also send peripheral borrowing costs spiraling. All this leaves us favoring credit over stocks and neutral on euro area government bonds.

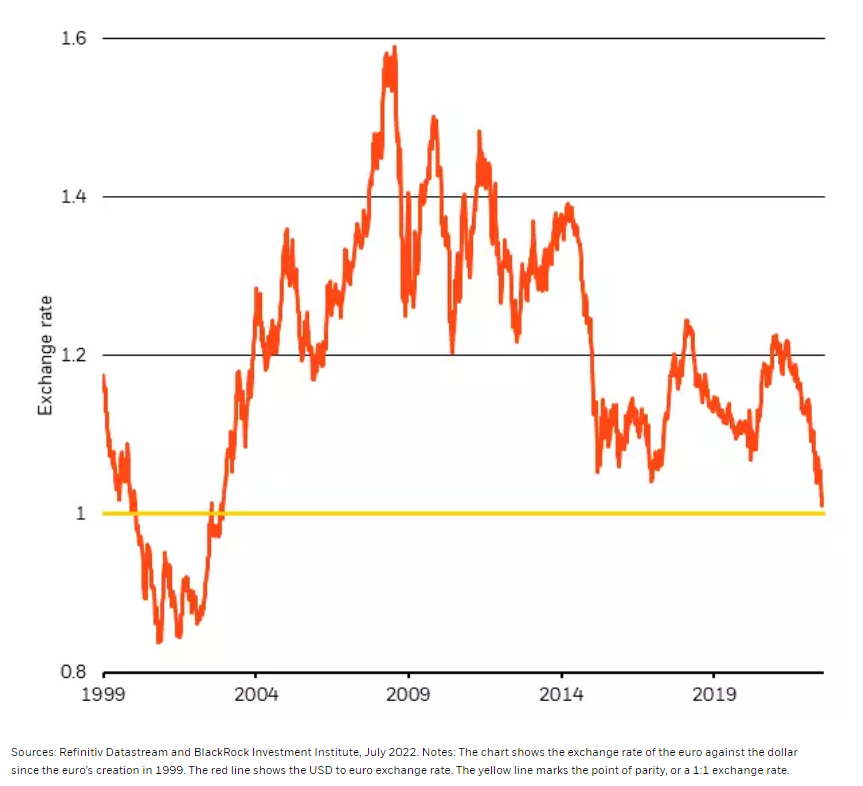

Parity pain

Euro to U.S. dollar

In a new regime of increased volatility, the ECB faces an even starker trade-off between crushing growth and living with inflation amid the energy shock. The central bank has yet to acknowledge this, in our view, as its forecast assumes inflation can come down in a growing economy. We think that’s unlikely – and see the euro area growth falling into recession even if rates rise only very little. Why? We’ve argued since right after Russia’s invasion of Ukraine that the energy shock will drag down economic activity. We see the ECB pausing when faced with rapidly slowing growth. Yet markets are still expecting significant hikes in the next year, Refinitiv data on futures pricing show. The dollar’s strength against the euro reflects the more pessimistic growth outlook for Europe, in our view. It’s near parity with the U.S. dollar, its weakest level in 19 years. See the chart.

Why is Europe’s growth slowing? Surging energy prices have heralded a recession in Europe since the invasion, as we said in A new supply shock. The impact on Europe is similar to the oil price shock in the 1970s, in our view. Europe’s reliance on imports means it’s more sensitive to higher energy costs than the U.S. Persistently high energy prices will likely squeeze real incomes, dampen business and consumer confidence as well as elevate financial stress. The drag on growth could be much bigger if Russia restricts supply, spurring rationing and production interruptions. Rationing is of particular concern for Germany, where some worry Russia may use pipeline maintenance as an excuse to cut off the flow of gas.

Peripheral stress

There’s another challenge weighing on the ECB: the risk of the euro zone fragmenting. High debt loads in peripheral nations such as Italy mean slowing growth and higher rates have contributed to widening yield differentials between peripheral bonds and their German counterparts. That prompted the ECB to plan to launch an anti-fragmentation tool: a program to purchase bonds from countries where borrowing costs deviate materially from the rest of the euro area. The ECB is set to give details this week. It hasn’t been easy historically to unite Europe around what is effectively sharing debt. The plan is likely to come with strings attached that could prove politically unpalatable for countries like Italy, where a brewing political crisis is adding to the stress. It’s also not clear when the ECB would use the tool.

Monetary policy can’t save the day, in our view. The ECB faces some brutal trade-offs to get inflation back down to target. We expect the ECB to raise rates out of negative territory to levels not seen since 2013. Yet the fallout of the energy shock and stress in peripheral bonds will force the ECB to pause its rate hikes sooner than the Fed, in our view. That ultimately means the euro area lives with more persistent inflation.

What this means for investments

Tactically, we’re underweight European equities because we see the energy shock stalling growth. We do see opportunities within sectors like healthcare that derive a large portion of revenues from U.S. sales. We favor credit instead amid higher yields and limited default risk. Overall, we dislike U.S. Treasuries and most other government bonds in this inflationary environment. We see the ECB pausing its hiking cycle sooner than the market expects, so we’re neutral on European government bonds. This includes peripheral bonds, even with the vulnerabilities. A key question there is whether markets are over- or underwhelmed by the scope and flexibility of the anti-fragmentation tool. Among global inflation-linked bonds, we prefer Europe. We believe the market underappreciates pressure from the energy crunch.

Market backdrop

Last week’s U.S. CPI data showed inflation reached fresh 40-year highs in June. This likely cements the case for a significant Fed rate hike at its policy meeting later this month, in our view. We also see elevated inflation persisting in Europe, bolstering the ECB’s decision to raise rates this week for the first time in over a decade. Markets showed high intraday volatility with stocks recovering most losses and long-term bond yields ticking lower as the euro leveled with the U.S. dollar.

This week’s focus is on the ECB monetary policy decision. We see the ECB raising interest rates by 0.25% amid persistently high inflation and despite growing recession fears. We also expect more details on the anti-fragmentation tool that’s intended to limit borrowing cost divergences. A series of PMIs will be a key gauge of economic activity around the world.

Week Ahead

July 19: UK labor market data

July 20: UK CPI; euro area consumer confidence

July 21: ECB, Bank of Japan rate meets; U.S. Philly Fed business index

July 22: U.S., euro area, UK, Germany PMIs

BlackRock’s Key risks & Disclaimers:

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of 18th July, 2022 and may change. The information and opinions are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This material may contain ’forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation. Investment involves risk including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are often heightened for investments in emerging/developing markets or smaller capital markets.

Issued by BlackRock Investment Management (UK) Limited, authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from BlackRock Investment Management (UK) Limited. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Investor Information Document (KIID), which may be obtained from MeDirect Bank (Malta) plc.