Wei Li, Global Chief Investment Strategist of the BlackRock Investment Institute together with Baeta Harasim, Senior Investment Strategist, Natalie Gill, Portfolio Strategist and Nicholas Fawcett, Macro Research all forming part of the BlackRock Investment Institute, share their insights on global economy, markets and geopolitics. Their views are theirs alone and are not intended to be construed as investment advice.

Key Points:

Equities over bonds – We prefer equities even as bond yields have sprinted higher. Global growth is still solid, and we see central banks ultimately living with inflation.

Market backdrop – U.S. 10 year yields hit new three year highs last week, and stocks fell. The European Central Bank affirmed our view it will normalize policy very slowly.

Week ahead – Sentiment data this week could show the economic impact of the tragic war in Ukraine. Chinese GDP data may indicate how lockdowns are affecting growth.

Bond yields have sprinted higher on ballooning inflation and hawkish comments by central banks. Yield spikes have often spelled trouble for stocks, but we believe the past is an imperfect guide in a world shaped by supply shocks. We see central banks normalizing quickly – but not slamming the brakes on the economy. This should keep real yields low and underpin equity valuations. The inflationary backdrop and growth momentum led by the U.S. also favors stocks, we believe.

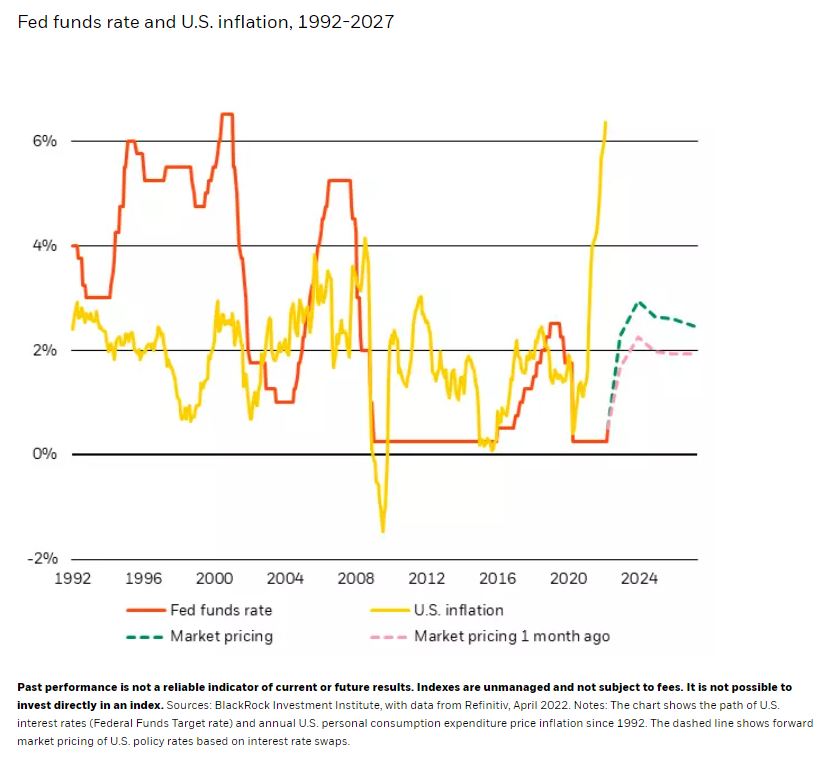

Historically low rates ahead

Yields on benchmark 10-year U.S. Treasuries hit three-year highs last week after data showed inflation was still running at levels not seen since the early 1980s. This understandably created angst about equities, especially about stocks of fast-growing tech companies. Higher discount rates make future cash flows less attractive. We believe fears about a further downdraft in equities are overblown. The rate hikes we expected are happening faster, but we don’t see central banks raising policy rates beyond neutral levels that neither stimulate or restrain the economy. Markets have priced in a rapid rise of the fed fund rate to 3% in the next year, followed by a leveling out to 2.5% in five years’ time (the green dotted line in the chart). That’s markedly higher than a month ago (dotted pink line), just before the Fed raised rates and started to talk tough on inflation. We don’t see the Fed going this high. Even if it did, the level would still be historically low compared with previous hiking cycles (red line) and the level of inflation (yellow line).

The big picture

Markets have swiftly brought forward a rise in policy rates in the past year and now are pricing in a steep lift-off. Yet it’s the sum total of rate hikes that matters for equities, in our view, not the timing and speed. Why? We use the cumulative rate for determining future corporate cash flows, not the current rate or bond yields. And the higher the peak rate in this cycle, the bigger the impact because of the compounding effect over time. As a result, we believe equities can thrive when the end destination of policy rates is historically low. Central banks will be forced to live with inflation, in our view, to avoid destroying growth and employment. We see inflation settling higher than pre-Covid levels because of the supply shocks triggered by the restart of economic activity and the horrific Ukraine war. This means real yields, or inflation-adjusted yields, should remain low and underpin equity valuations. We could see long-term yields rising further as investors demand higher compensation for holding them in the inflationary backdrop. This is not necessarily bad news for equities as it could trigger a re-allocation away from bonds into equities.

How about equity fundamentals? Three things jump out at us as first-quarter results get underway this week. First, the powerful restart is providing a growth cushion for developed markets (DM economies), especially in the U.S. Second, record-high profit margins bear close watching. DM companies have been able to pass on increased input costs to consumers and kept labor costs in check – so far. Third, we see the economic fallout of the Ukraine war cutting into earnings even as analysts have been revising up estimates across the board. We expect estimates for European companies to come down in particular as analysts start factoring in the war’s effects. Companies in the MSCI Europe index are export-oriented and derive just half of their revenues domestically, we calculate, softening the impact a bit. A weaker euro helps, too. All in all, this led us to reduce our overweight in European equities earlier this month. We prefer U.S. and Japanese equities instead.

What are the risks? First, central banks could trigger a recession by raising rates too high in an effort to contain inflation. Second, inflation expectations could become de-anchored from central bank targets and cause them to slam the brakes. Third, companies could see margins shrink amid escalating input costs and upward wage pressures.

The bottom line

We prefer DM equities in the inflationary backdrop of the restart’s momentum and a historically low sum total of rate hikes. We could see long-term yields rising further as investors demand a higher term premium, or extra compensation for holding them amid high inflation and debt levels.

Market backdrop

Yields of 10-year U.S. Treasuries hit new three-year highs last week, and stocks fell. We believe long-term yields can rise further and could see short-term bonds outperforming because market expectations for rate increases have become overly hawkish. The European Central Bank confirmed our view it will normalize slowly and gradually. It’s set to end asset purchases in the third quarter and raise its policy rate “some time” thereafter.

We are focusing on sentiment data this week as investors gauge the economic impact of the war in Ukraine. Supply shocks caused by the conflict and pandemic will hit European activity, in our view, while U.S. activity should stay robust. China GDP data will give an early read on growth amid concerns around the impact of renewed lockdowns amid a spike in COVID cases.

Assets in Review

Week ahead

- April 18: China Q1 2022 GDP, retail sales, industrial output and urban investment data

- April 19: IMF World Economic Outlook and updated forecasts

- April 20: Euro area consumer confidence flash; U.S. Philly Fed Business Index

- April 22: Japan CPI; Japan, Germany, Euro area and U.S. flash PMIs

BlackRock’s Key risks & Disclaimers:

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of February 28th, 2022 and may change. The information and opinions are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This material may contain ’forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation. Investment involves risk including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are often heightened for investments in emerging/developing markets or smaller capital markets.

Issued by BlackRock Investment Management (UK) Limited, authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from BlackRock Investment Management (UK) Limited. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Investor Information Document (KIID), which may be obtained from MeDirect Bank (Malta) plc.