Jean Boivin Head of the BlackRock Investment Institute together with, Wei Li, Global Chief Investment Strategist, Alex Brazier, Deputy Head and Vivek Paul, Head of Macro Research all forming part of the BlackRock Investment Institute, share their insights on global economy, markets and geopolitics. Their views are theirs alone and are not intended to be construed as investment advice.

Key Points

Forum lessons: BlackRock’s top investment leaders came together at the Outlook Forum. The upshot: The new regime is not about to change, and we need a new playbook.

Market backdrop: Stocks slid and yields rose as the Federal Reserve delivered another mega rate rise and signaled it would need to take rates even higher than originally planned.

Week ahead: U.S. inflation is in focus this week after the jobs data showed ongoing worker shortages. We don’t think the data will deter the Fed from overtightening.

We see the new regime of greater macro and market volatility playing out. This backdrop made for a spirited Nov. 1-2 Forum, a semiannual gathering of BlackRock’s top investment leaders to debate the outlook. We think this new regime is not about to change, and debated how to navigate a recession foretold, persistent inflation, geopolitical fragmentation, a strong U.S. dollar and the energy crunch.

Wishful thinking on inflation

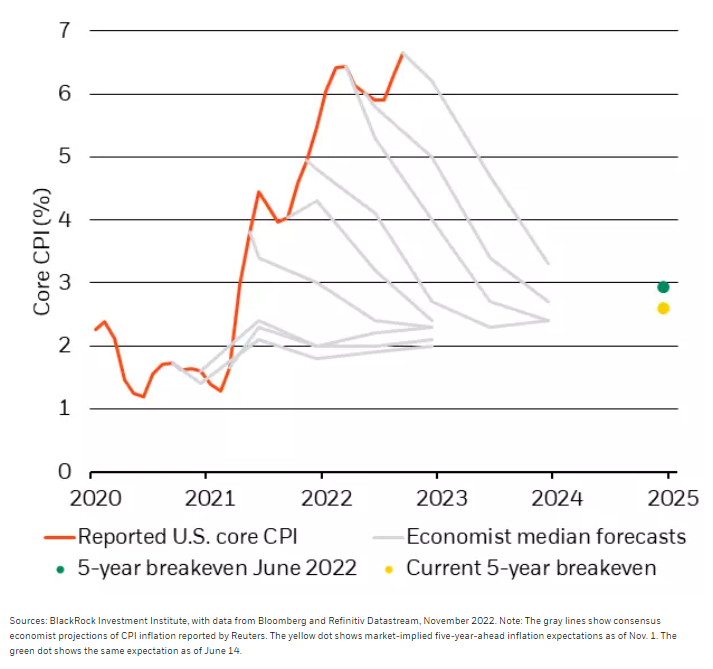

Core CPI inflation, forecasts and breakeven rates, 2020-2025

The constant upside surprises in inflation relative to median forecasts (gray lines) are at the heart of market volatility – and underscore that we are in a new regime of greater macro and market volatility. Market pricing (green and yellow dots in chart) shows markets continue to expect a normalization of inflation. We think core inflation will be sticky primarily due to ongoing production constraints, especially in the labor market. Those constraints mean economies are overheating, even though activity hasn’t reached its pre-Covid trend. Central banks are set to overtighten, pushing economies into moderate recessions. But a deep recession is coming if central banks insist on bringing inflation fully back down to target as quickly as they typically aimed to do in the past.

We see the new regime playing out. Central banks face sharper trade-offs between activity and inflation. For now, we see them on a path to overtighten and cause recessions while attempting to bring inflation back to target. A resilient economy only makes further overtightening more likely, in our view, and would be even worse for the economy – and bad news for risk assets. The risk of financial cracks is also real. We think central banks will eventually pause their hikes once confronted with the economic damage they’ve caused. That would mean living with some higher inflation if production capacity doesn’t come back quickly.

Drivers of the new regime

The new regime is not about to change, in our view – reinforced by three big transitions that mean repeated drags on production capacity and thus persistent inflation. First, aging populations are limiting the number of working-age people and will place pressure on public finances. Second, we think the era of great geopolitical moderation has ended, leading to a persistent geopolitical risk premium, exemplified by rewiring global supply chains and strategic competition between the U.S. and China. This is the most fraught environment we have seen in the world in the post-World War Two era. Third, we see the transition to net-zero carbon emissions reshaping energy demand and supply over time.

So how should investors adjust to all this? The new regime needs a new investing approach. We think ongoing sizing of what’s in the price of a given asset is crucial. It will matter more than trying to time a sustained bull market, in our view. Investors learned it paid to “buy the dip” during the bull markets of the “Great Moderation,” a multidecade period of stable growth and inflation that is over now. The urge is still there, much like all characters in The Lord of the Rings are drawn to the power of the One Ring – but what promised gains before now promises pain, we think. We must avoid the ring’s temptation – the old playbook – to buy dips or time rallies. Doing so risks ruining one’s life, like Gollum, or one’s portfolio in the new regime. This is true for stocks as well as bonds. Central banks are hiking rates and causing recessions, not responding to them by cutting rates. So we think long-term government bonds won’t offset risk asset selloffs like they did in past recessions.

Our bottom line

The new regime is here to stay. We need to make more frequent portfolio changes and plan for more granular allocations to pounce on opportunities – and avoid the temptations of the One Ring. In the near term, attractive yields on short-term credit make it an appealing place to wait out the coming recession, we think. We don’t think equities have fully priced recession risks – and earnings forecasts still look too optimistic.

Market backdrop

Stocks slumped and short-term U.S. Treasury yields hit 15-year highs after the Federal Reserve delivered another mega rate hike, as expected, but also signaled it would have to take rates higher than it originally planned, even if at a slower pace. Markets were disappointed again as the dovish signal they were hoping for failed to materialize, snuffing out an equity bounce. We see the Fed on a path to overtighten policy and don’t expect it to pause until the damage caused is clearer.

Markets will keenly watch the U.S. CPI for any signs of easing inflation. Persistently high inflation could embolden the Fed to hike rates even more than the market expects. Consumer sentiment may give a sense of the economic damage inflicted by the Fed’s tightening, and the report will also show the latest snapshot of household inflation expectations.

Week Ahead

Nov. 7: UK house prices; German industrial production

Nov. 8-9: Japan trade data; China CPI

Nov. 10: U.S. CPI

Nov. 11: UK GDP; U.S. University of Michigan consumer sentiment

BlackRock’s Key risks & Disclaimers:

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of 7th November, 2022 and may change. The information and opinions are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This material may contain ’forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation. Investment involves risk including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are often heightened for investments in emerging/developing markets or smaller capital markets.

Issued by BlackRock Investment Management (UK) Limited, authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from BlackRock Investment Management (UK) Limited. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instruments discussed in the document may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest in a mutual fund should always be based upon the details contained in the Prospectus and Key Investor Information Document (KIID), which may be obtained from MeDirect Bank (Malta) plc.