Liontrust GF High Yield Bond Fund is manufactured by Liontrust Fund Partners LLP and represented in Malta by MeDirect Bank (Malta) plc.

Market review

The global high yield market returned 1.5% (US dollar terms) in the second quarter of 2024. The US high yield market produced a return of 1.1% while in Europe the market returned 1.9% during the period. The returns across the different rating bands in US and Europe were broadly similar, although European CCCs produced an impressive return of 3.9%, while US CCCs were fairly anaemic at 0.2%.

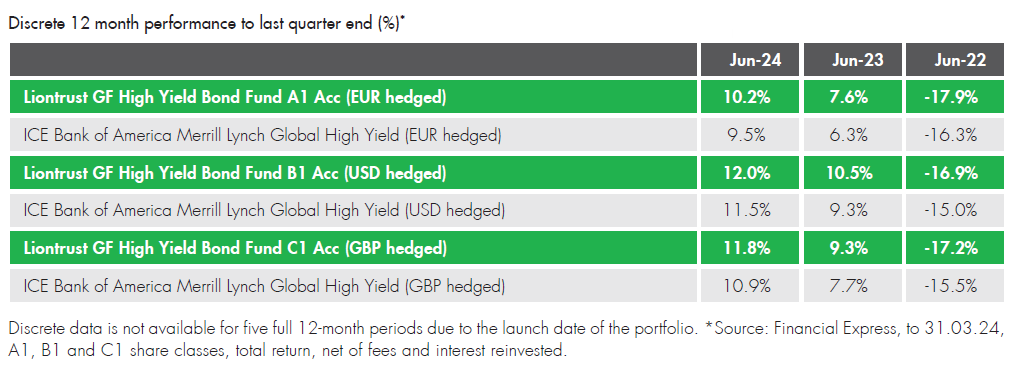

Fund performance

With its index matching returns in the quarter, the main positive contributors in the Fund included Ceramtec, a ceramic products manufacturer, and Grifols, a blood plasma producer. Both are CCC rated, euro denominated bonds and therefore perhaps tapping into the broader them of euro CCC outperformance.

Grifols was a topical bond in Q1 for its underperformance, but during Q2 it made progress in the refinancing of its capital structure, including asset sales. We sold out of the position towards the end of the quarter after the bond was downgraded to Caa2. The positive contribution of this bond was dimmed a little by this rating action, but the general view held by Moody’s is the company now has a large amount of strategy execution risk in order to deliver its balance sheet. We agree with this assessment and felt selling the bond at a price in the low 80s was prudent whilst we wait for more evidence that, operationally and financially, the company is on the right path. Another company, B-rated Saga Plc, contributed positively as it made progress in refinancing its bonds, when previously the market had shown a little scepticism – undue in our eyes – that its 2024 bond would be refinanced.

Less positively, an example of poor stock-picking in the quarter was in another CCC-rated euro-denominated bond, Kloeckner Pentaplast. This was a very small position size due to its relatively precarious position versus a 2026 maturity wall. We decided to exit this small position at a price close to 50 as, effectively, we lost conviction that par is the likely outcome for this bond. During the quarter (and indeed the year to date), the holding cost the fund only a few basis points, and the cost to the fund over the entire holding period was less than 10bps, due in large part to some good trading, sensible position sizing and, of course, carry.

No particular sector stands as out as driving marked relative returns during the quarter. Real estate felt somewhat quiet, certainly relative to recent quarters, though still made the Fund a relative return of close to 20bps. Aroundtown, added to the Fund in January, and long-term holding CPI Property were the main contributors, although CPI’s contribution would have been greater had it not been downgraded to sub-investment grade during the period. We took the opportunity to top up its senior unsecured bonds in the aftermath of this downgrade.

Trade activity

The Fund invested in a new holding during the quarter called Brightline East. This is an extremely unique company in the high yield market, where it has built ‘higher speed’ rail in Florida and is now going through the ramp-up phase whilst Floridian travellers increase their use of this new service. It has a coupon of 11%; we bought it below par and the bond structure comes with a couple of years of debt service reserves whilst ridership grows. This is a different proposition to what we have in the portfolio, is highly idiosyncratic and we believe paying well for what are clear risks.

Elsewhere we participated in a new issue by an auto parts company called Mahle. This German company is owned by a foundation, which extracts only very modest dividends for charitable use. We think it is managed with a long-term outlook and has a balance sheet to cope with the natural cyclicality in the autos market.

Outlook

Sticky inflation continues to drive volatility in rates markets, whilst credit markets remain extremely resilient. Whilst unemployment remains low, credit conditions are fairly benign, so we do understand why High Yield has generally been stable. Yet the longer rates remain elevated, the risk of economic slowdown further down the line increases. In this context, we have been happy to gradually reduce risk in the portfolio. We believe we are prudently positioned for what we believe to be a somewhat precarious macro back-drop, though still harvesting the now attractive income being generated by the asset class.

The Fund continues to invest in bonds based on strong corporate fundamentals and has a bias towards high quality defensive credits, with minimal exposure to cyclical credits. We believe our defensive approach stands us in good shape to perform if and when default risk is the major driver of the market, rather than interest rates. The Fund is currently offering yield of around 9.1% for sterling investors (and around 7.5% for euro investors), which we view as an attractive entry point.

Liontrust Key risks & Disclaimers:

Past performance is not a guide to future performance. Do remember that the value of an investment and the income generated from them can fall as well as rise and is not guaranteed, therefore, you may not get back the amount originally invested and potentially risk total loss of capital.

The issue of units/shares in Liontrust Funds may be subject to an initial charge, which will have an impact on the realisable value of the investment, particularly in the short term. Investments should always be considered as long term.

Investment in the GF High Yield Bond Fund involves foreign currencies and may be subject to fluctuations in value due to movements in exchange rates. The value of fixed income securities will fall if the issuer is unable to repay its debt or has its credit rating reduced. Generally, the higher the perceived credit risk of the issuer, the higher the rate of interest. Bond markets may be subject to reduced liquidity. The Fund may invest in emerging markets/soft currencies and in financial derivative instruments, both of which may have the effect of increasing volatility. The Fund may invest in derivatives. The use of derivatives may create leverage or gearing. A relatively small movement in the value of a derivative’s underlying investment may have a larger impact, positive or negative, on the value of a fund than if the underlying investment was held instead.

Issued by Liontrust Fund Partners LLP (2 Savoy Court, London WC2R 0EZ), authorised and regulated in the UK by the Financial Conduct Authority (FRN 518165) to undertake regulated investment business.

This document should not be construed as advice for investment in any product or security mentioned, an offer to buy or sell units/shares of Funds mentioned, or a solicitation to purchase securities in any company or investment product. Examples of stocks are provided for general information only to demonstrate our investment philosophy. It contains information and analysis that is believed to be accurate at the time of publication, but is subject to change without notice. Whilst care has been taken in compiling the content of this document, no representation or warranty, express or implied, is made by Liontrust as to its accuracy or completeness, including for external sources (which may have been used) which have not been verified. It should not be copied, faxed, reproduced, divulged or distributed, in whole or in part, without the express written consent of Liontrust. Always research your own investments and (if you are not a professional or a financial adviser) consult suitability with a regulated financial adviser before investing.

MeDirect Disclaimers:

This information has been accurately reproduced, as received from Liontrust Fund Partners LLP. No information has been omitted which would render the reproduced information inaccurate or misleading. This information is being distributed by MeDirect Bank (Malta) plc to its customers. The information contained in this document is for general information purposes only and is not intended to provide legal or other professional advice nor does it commit MeDirect Bank (Malta) plc to any obligation whatsoever. The information available in this document is not intended to be a suggestion, recommendation or solicitation to buy, hold or sell, any securities and is not guaranteed as to accuracy or completeness.

The financial instrument discussed in the document is intended for retail clients however, it may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein.

If you invest in this product you may lose some or all of the money you invest. The value of your investment may go down as well as up. A commission or sales fee may be charged at the time of the initial purchase for an investment. Any income you get from this investment may go down as well as up. This product may be affected by changes in currency exchange rate movements thereby affecting your investment return therefrom. The performance figures quoted refer to the past and past performance is not a guarantee of future performance or a reliable guide to future performance. Any decision to invest should always be based upon the details contained in the Prospectus and Key Information Document (KID), which may be obtained from MeDirect Bank (Malta) plc.